The South African Consumer Landscape

Introduction

In this chapter, we survey the South African consumer landscape from a demographic and consumer segment perspective. For marketers, it is always good practice to try to understand the consumer landscape in a particular country. This can help provide answers to some important questions, such as, what is the size of the market? How many consumers can afford to buy a certain product or service? Where are consumers located?

Understanding the consumer landscape in South Africa is a big challenge for marketers. Our ever-changing consumer market is unique, often bearing only a limited resemblance to the rest of the world. In this chapter, we provide a window on how the South African consumer landscape is structured as well as some of the key developments over recent years.

Basic demographics

South Africa's population is the 24th largest in the world [1] with approximately 58 million people [2]. We rank just below Italy and just above Tanzania. The country's population continues to grow, with around 2000 new babies born every day. Unlike many other developing countries, the rate of population growth is slowing (highlighted by a decline in the fertility rate). In 2009, South African women bore an average of 2.66 children. By 2018, this had declined to 2.4.

Over recent decades, life expectancy in South Africa has increased dramatically. In 2006, life expectancy for South African men was 52 years, but by 2018 this had risen to 61 [3]. Similarly, in 2006 the life expectancy for women was 62, but by 2018 this had risen to 67 [4]. There are a number of factors driving this dynamic, including better healthcare, which has resulted in both a reduction in infant mortality and HIV/AIDS-related deaths. Figure 5.1 shows a comparison of median ages (i.e. 50% of the population will be older and 50% of the population will be younger) for Nigeria, South Africa and Japan. The graphic shows that South Africa has a relatively young median age (26) compared to Japan (46), but not as young as Nigeria (18).

Figure 5.2 shows a population pyramid for the same three countries (Nigeria, South Africa and Japan). These three pyramids show that most of Nigeria's population is very young and the opposite is true for Japan. South Africa has a similarly young 'bulge' at the bottom of the pyramid.

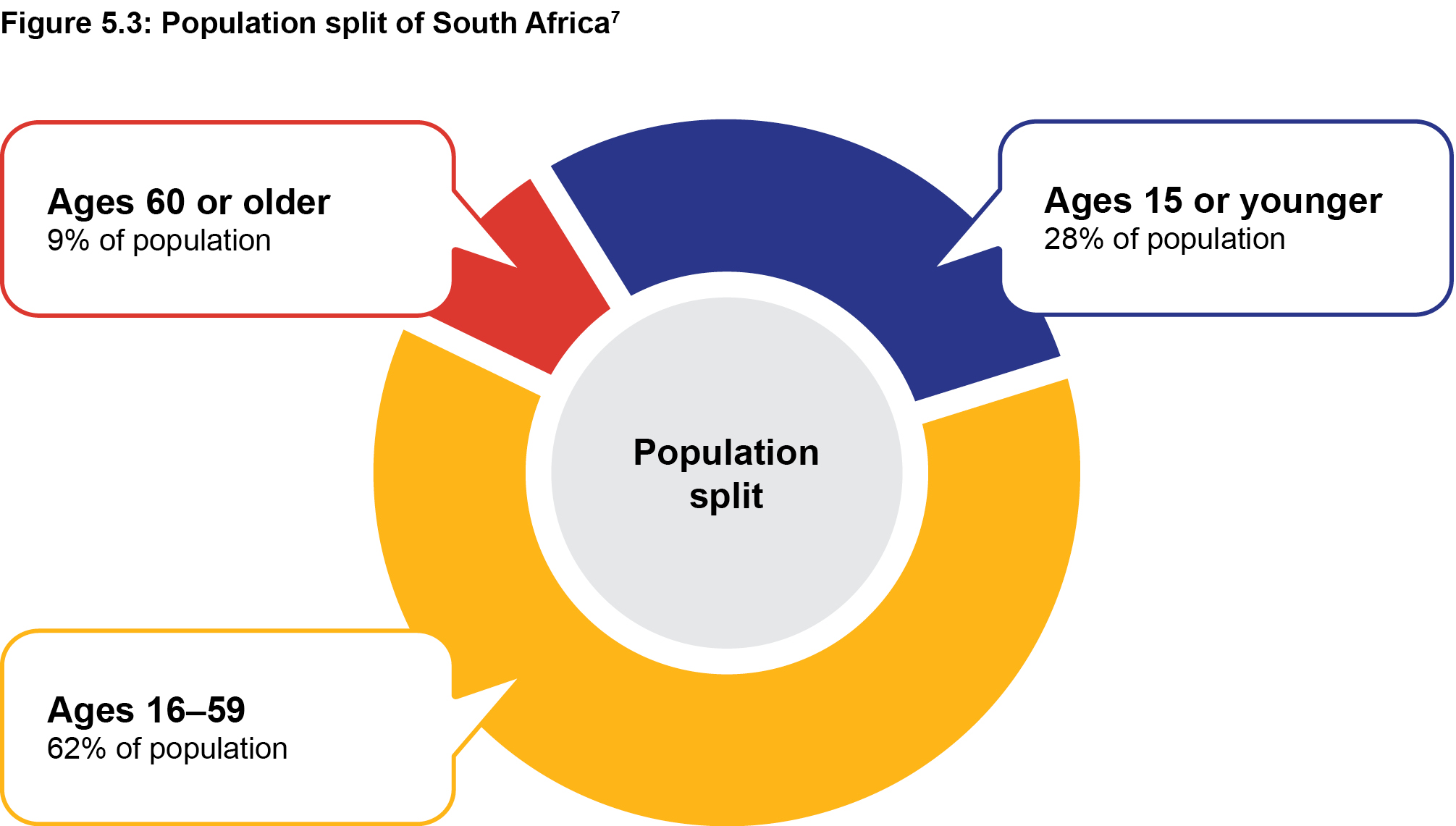

A more detailed population split of the South African consumer landscape is shown in Figure 5.3. The figure shows that 28.8% of the population is 15 years old or younger (a 'child', according to the United Nations classification); while 9% of the population is over 60 and the balance (62.3%) are working age.

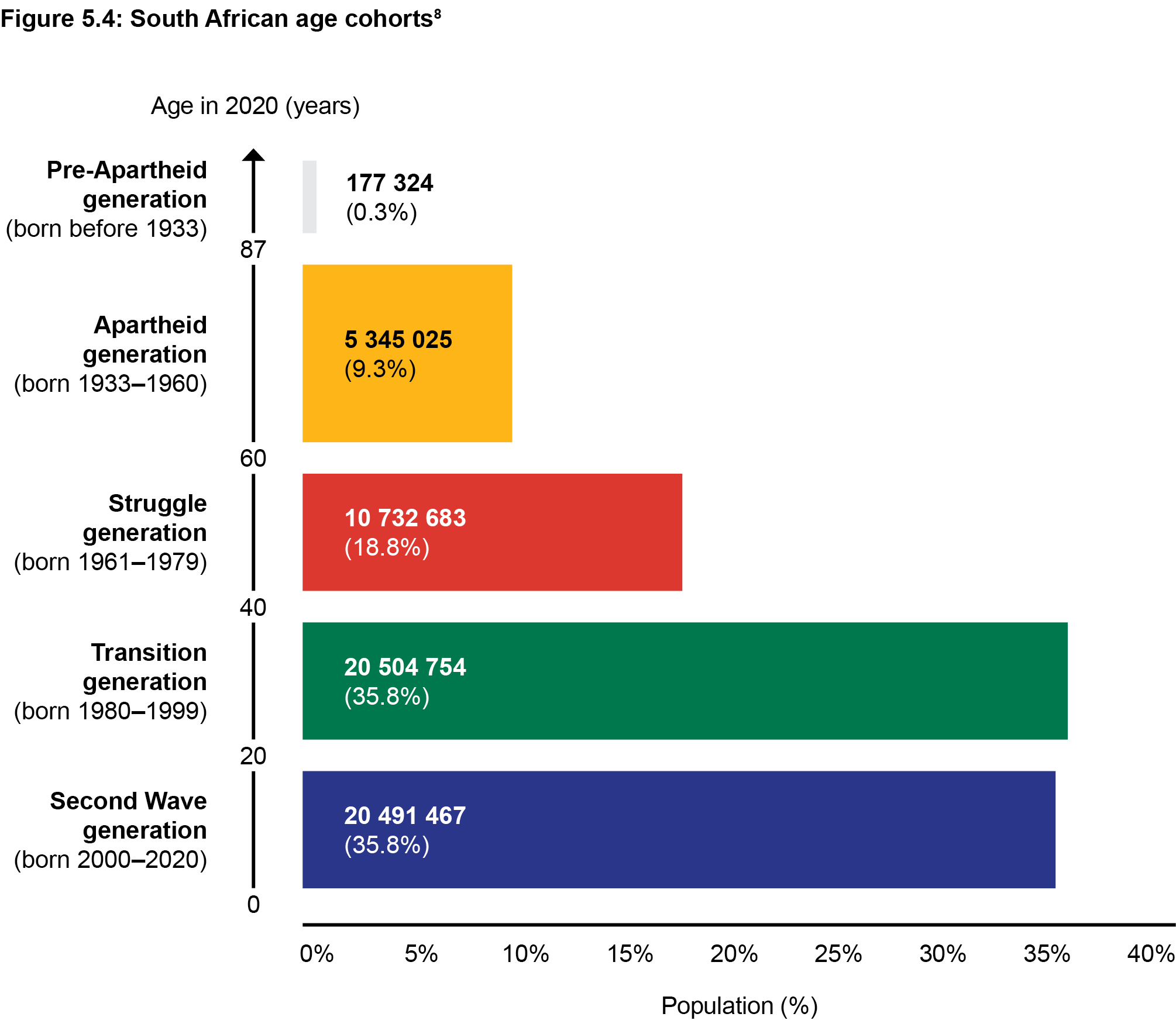

The use of generational cohort theory is common in marketing in order to separate one generation from another. Many marketers will use terms like baby boomers, Generation Z or millennials to describe their target markets. Most of these terms do, however, have strong roots in historical events which took place in the Global North. The term baby boomer, for instance, comes from the generation that was born post-World War II, after millions of families had lost members during the war. In South Africa, we have our own history. World War II ended at the same time that the National Party took power in South Africa and Apartheid officially started. Using terms from the Global North to describe the South Africa context can therefore be problematic. Figure 5.4 provides a South African framework for segmenting by age cohort.

Each of these cohorts can be described as follows:

- Pre-Apartheid generation: Born before 1933 and grew up in the pre-Apartheid era. Racial segregation existed, but was not codified to the extent that it was under formalised Apartheid.

- Apartheid generation: Born between 1933 and 1960, this generation grew up in the early, core Apartheid regime (before the tide started to shift due to the Sharpeville massacre in 1960).

- Struggle generation: Born between 1961 and 1979. After Sharpeville, the struggle for democracy shifted and a more coordinated effort was sustained to push for reform.

- Transition generation: Born between 1980 and 2000. Growing up during the twilight of Apartheid and transitioning into an official post-colonial South Africa. The latter group in this cohort was born during democracy.

- Generation second Born after 2000. Having never seen Apartheid first-hand, this generation is the second wave of youth born into democracy.

While age is a useful segmentation tool, the model presented here needs further exploration in order to account for economic inequality and differences between population groups. For example, the past and current lived experience of a Black member of the struggle generation is very different to a white member of the same generation. Inequality and racial differentials must always be applied to understanding South Africa, given the county's past and current population composition.

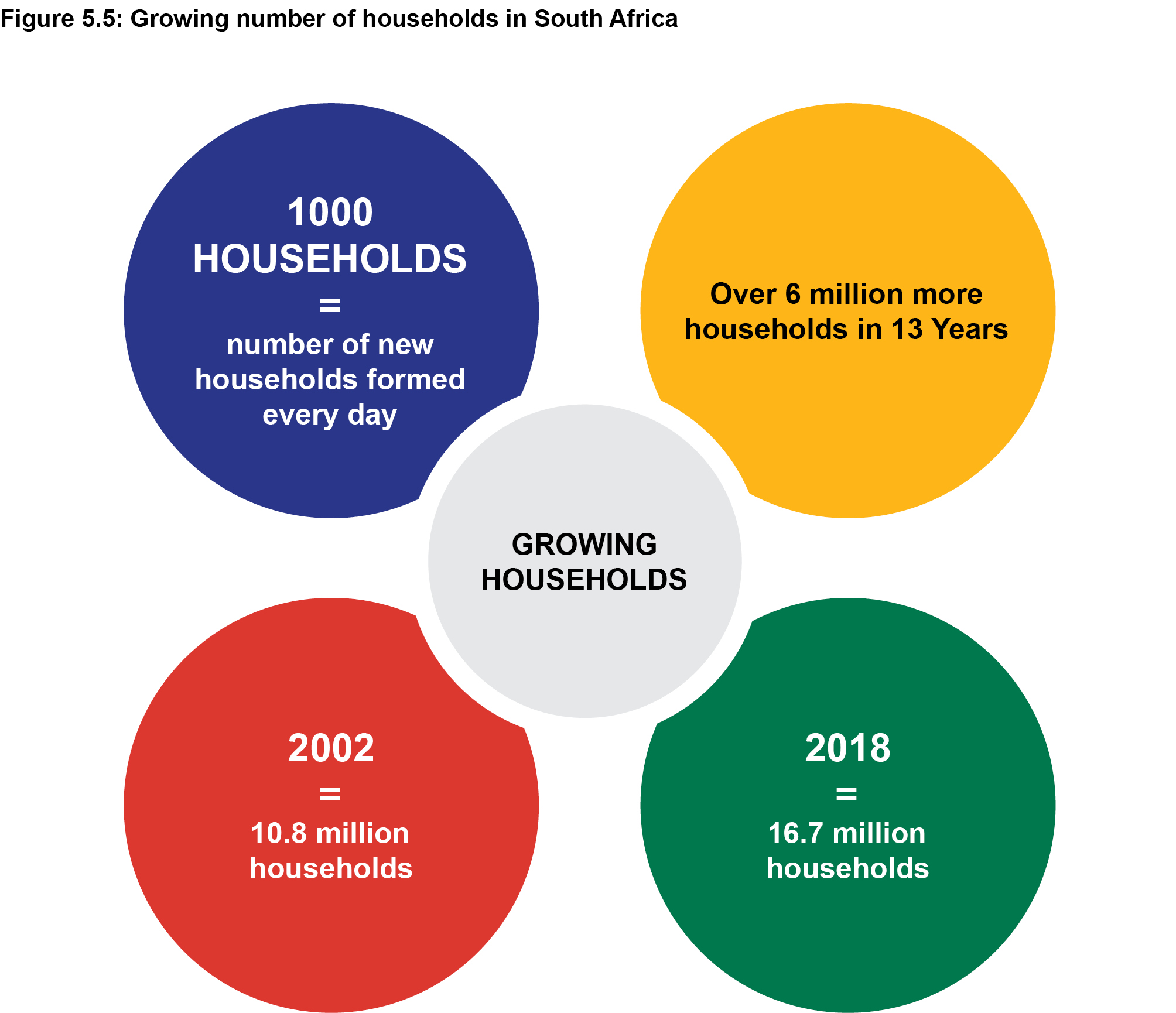

South Africa's population is expected to increase to 65–67 million people by 2030, and to 75–78 million by 2055 [9]. Due to the growth in population over the last two decades, the number of households has increased by around 1000 per day, with over 6 million households being added from 2002 to 2018, as illustrated in Figure 5.5.

While demographics can be more granular, the data presented here provide a broad overview of how large the South African consumer population is. The next section provides some context in terms of where South African consumers live.

Where do South Africans live?

As a developing country, South Africa has seen rapid urbanisation over recent decades. Roughly 63% of South Africans now live in urban centres and this is expected to rise to over 70% by 2025 as more people flood into the cities in search of work opportunities and better facilities, such as schools for their children [10].

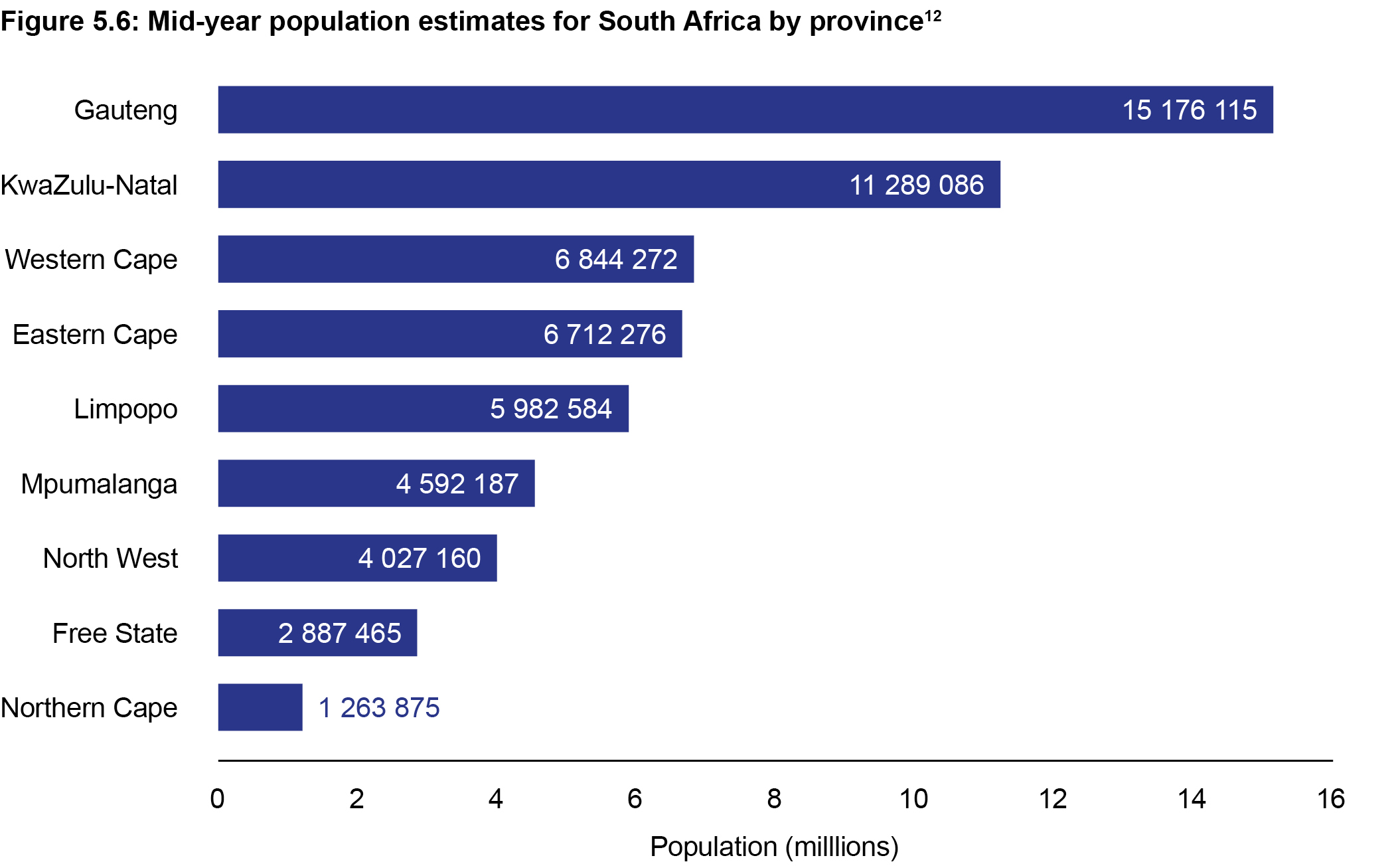

With a gross domestic product that is larger than that of most African countries, Gauteng is South Africa's economic hub. Unsurprisingly, it is also the most populous province, with one in four South Africans living there. In contrast, despite being larger in size, the Northern Cape is the least populated province, with just 2% of South Africans living there [11]. Figure 5.6 provides a full provincial population breakdown.

When categorising where people live, there are a number of terms used in the study of populations and urbanisation. Major categories include:

- Urban: A heavily built up area, such as a city or town.

- Peri-urban: An area immediately next to a city or town.

- Rural: Refers to the countryside and an area away from a city or town.

Each of the above types of setting provides different opportunities and challenges for consumers and those attempting to meet their needs. For example, distributing food to rural areas is much more expensive because of the distances that need to be travelled. Urban areas are usually higher in population density and consumers are better positioned to access a wider array of products and services.

South African consumers by race and language

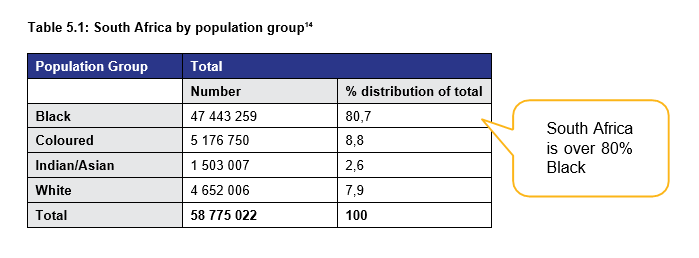

Over 80% of South Africa's population is Black. Table 5.1 shows the breakdown of population groups, with around 81% of South Africa's population being Black, 9% Coloured, 8% white and 2% Indian/Asian [13].

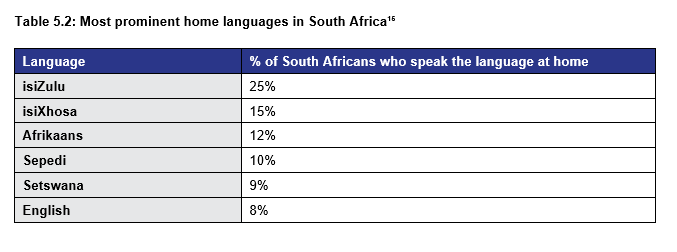

There are 11 official languages in South Africa and isiZulu is by far the most spoken home language. Table 5.2 shows some of the more prominent first languages in South Africa. Note that less than 10% of South Africans have English as their home language in spite of it being the dominant language for formal business.

The breadth of home languages provides marketers with a challenge when it comes to marketing communications (see Chapter 16). South Africa does not just have a disparate language landscape, but there is great economic disparity, as discussed in the next section.

Economic disparity

Inequality is arguably the most glaring characteristic of the South African consumer landscape. According to the United Nations, South Africa is regarded as one of the most unequal countries on earth. Income disparities are measured using a formula called the Gini coefficient. South Africa has a Gini coefficient of over 0.60, which is one of the highest in the world. Inequality in terms of wealth is even higher. In 2015 the richest 10% of South Africans held around 71% of net wealth, while the bottom 60% held a mere 7% of the net wealth [16].

For marketers, this presents a unique challenge. The head of a large consumer-facing company recently stated that marketing in South Africa is like operating in Bangladesh and Australia at the same time. This means that marketers need different strategies for the different consumer markets in South Africa. Most South Africans cannot afford iPhones, so there is little point in spending money advertising iPhones to the so-called mass market. On the other hand, there are millions of poorer South African households who do not have electric stoves or microwaves. Marketers selling food products to this consumer segment therefore have to think about the conditions under which food is prepared. Getting to grips with such diverse markets is crucial for marketers in understanding consumer behaviour.

Segmenting the South African consumer landscape

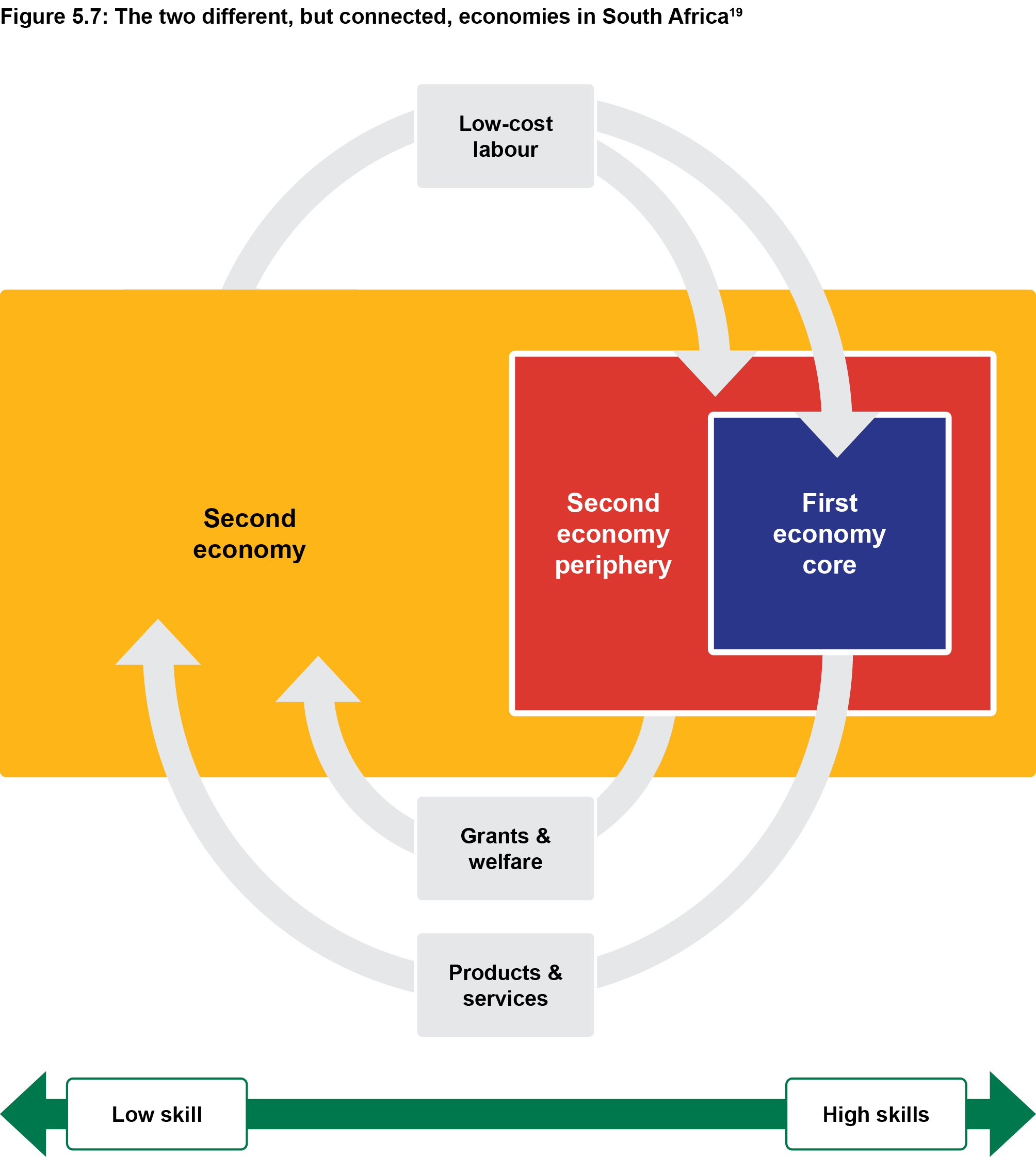

Former South African president Thabo Mbeki argued that South Africa had two economies [17]. On the one hand, South Africa possesses a sophisticated formal economy dominated by large corporations, similar to what one would find in the United States or Europe. At the same time, there exists a second economy, which is dominated by the informal sector. The informal sector includes everything from spazas to hawkers and employs more people than mining.

Both sectors are connected (see Figure 5.7). For example, goods and services produced in the formal sector are sold in the informal. What is clear is that those South Africans who work in the formal sector are typically much more skilled and are therefore inevitably much better off financially. At the other end of the spectrum are South Africans who are below the poverty line and are largely marginalised, with much lower incomes.

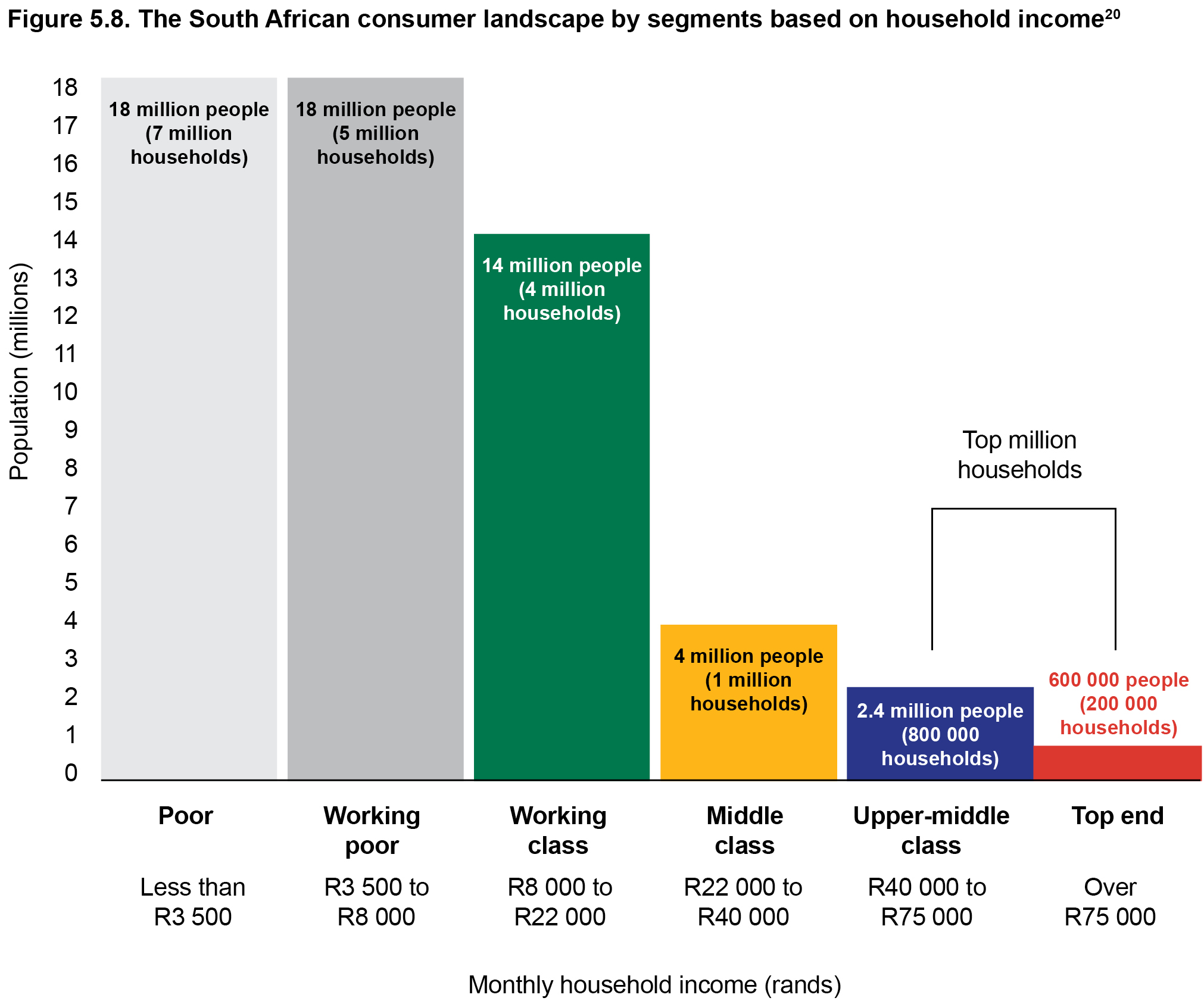

A powerful way to get a picture of the South African consumer landscape is to break up the South African population by household income. Using one simple variable, we are able to access a picture of the consumer landscape using the National Income Dynamics Survey (NIDS) data [18]. Figure 5.8 presents the household income of South Africa's population in six groups. The segment titled Poor shows that 18 million people live in households earning less than R3500 per month. The segment titled 'Top end' shows there are 600 000 people living in households earning over R75 000 per month.

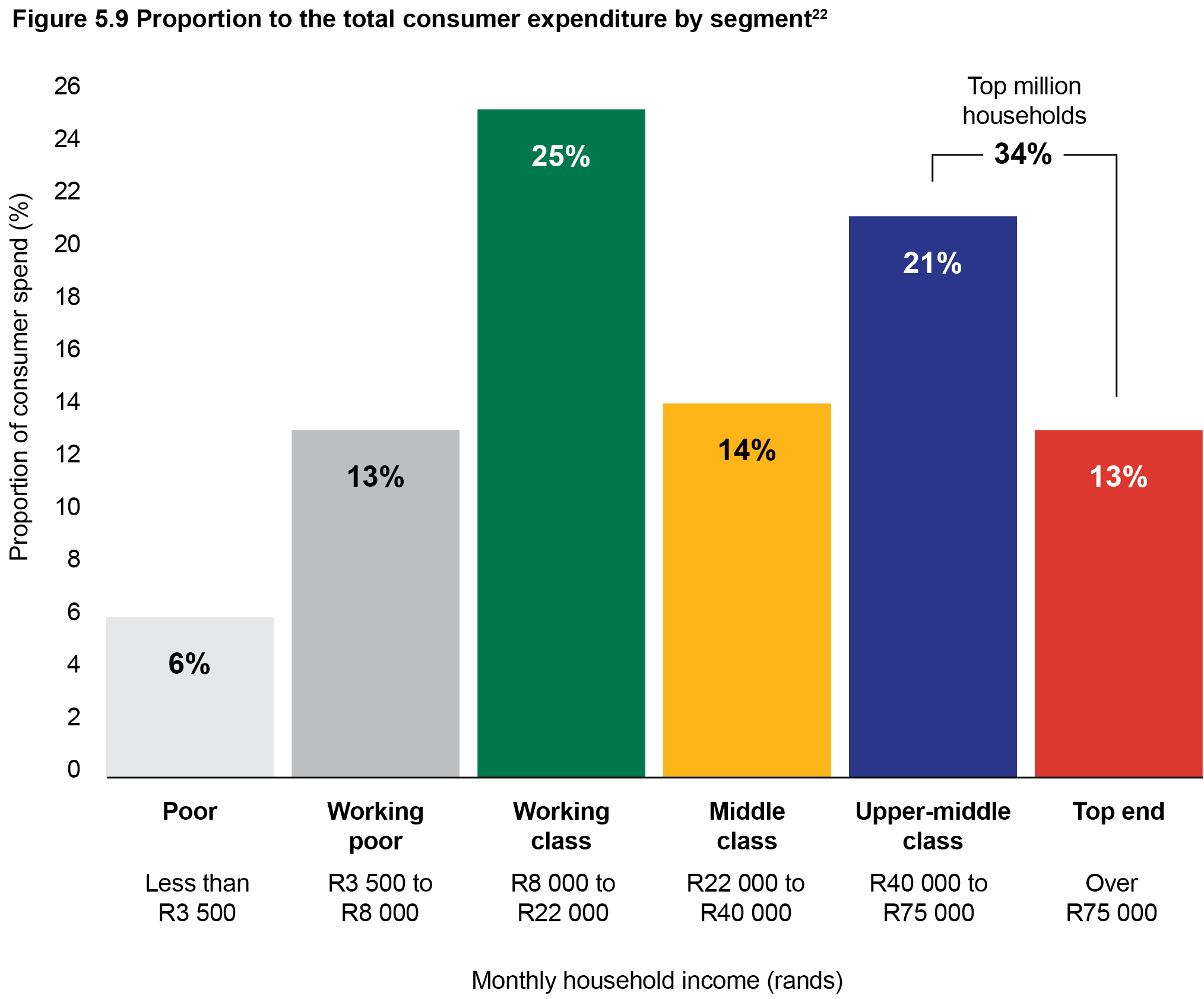

In the same way that each of the segments has a different size, they also have a different proportion of South Africa's total consumer expenditure. In Figure 5.9, each segment is shown in proportion to total consumer expenditure.

Even though the Poor households include nearly a quarter of South Africans, these households only account for 6% of overall consumer spending power. This is in sharp contrast to the 'Top end' who only make up just over 1% of the entire population, but account for 13% of all consumer spend.

In the next sub-sections, each of the household income segments in the figures above is explained and defined. This provides a foundation for further segmentation, as discussed in Chapter 11. All the data for these segments is sourced from NIDS (2019) [21].

Poor

The 'Poor' segment includes everyone living in households earning less than R3500 per month, which is the threshold to qualify for a government RDP house or housing subsidy. Over 7 million households, around a third of all South Africans, can be defined as Poor. Despite being the second-largest consumer segment, the Poor only account for 7% of all South African consumer spend.

Unemployment is endemic, with over half of all Poor households being without an adult who is employed. This means that there is a heavy reliance on government grants, especially child-support grants and old-age pensions. Those who are working typically work in the informal sector where wages are low and the practice of workers' rights is largely non- existent.

The Poor also represent the biggest segment in every province except Gauteng. However, there are more Poor households in Gauteng (South Africa's most populous region) than any other province. Due to the heavy reliance on grants, much of the spending by this segment occurs at month end. Indeed, buying behaviour varies significantly throughout the month, with bulk buying typically concentrated at the end of the month and top-up purchasing of basics being more common throughout the rest of the month.

Working poor

The 'Working poor' group comprises those South Africans living in households earning R3500–R8000 per month. R8000 is the cut-off point for qualifying for a child support grant in South Africa. This group constitutes the biggest consumer segment, with over 18 million people. Although the group make up nearly a third of all South Africans, they only are only responsible for less than 15% of all consumer spend. Levels of unemployment are significantly lower than the Poor, with 20% of households being without an adult who is employed. However, of those working, most are employed in low-skilled positions. Despite earning more than the Poor, the Working poor segment is still under immense financial pressure. This means that prices are scrutinised and budgets carefully managed. Many households closely examine specials in advance of carefully planned month-end shopping trips.

Working class

The 'Working class' earn R8000–R22 000 per month. They account for about 20% of all South African households and for a quarter of all consumer spend. This segment is often referred to as the 'Gap Market'. This is because people in this group fall into the gap between qualifying for a traditional government housing scheme and having sufficient income to secure loans from the private sector to buy property.

The government has tried to address this problem by implementing a Gap Market Housing Subsidy to help households which earn less than R22 000 per month. Unemployment in this group is relatively low (14%), with nearly 40% of those working in positions that require a high level of skill. It is not only in the context of housing in which this group falls into the proverbial gap. Medical aid and education are other categories where a large portion of this segment is not able to afford private-sector alternatives. However, there are many examples of businesses developing affordable medical and education products for this market.

Middle class

The 'Middle class' group includes households earning R22 000–R40 000 per month. Although the group is four-and-a-half times smaller than the Working poor segment, their combined spending power is greater. This group also has a greater likelihood of having more than one earner in the household (42%). A characteristic of this group, compared with poorer segments, is that they are likely to possess a high level of education. Over 50% of households contain an adult with a tertiary qualification.

Furthermore, while poorer segments are overwhelmingly Black African, nearly 50% of this segment is made up of other races. This group is more likely to have access to private vehicles than the poorer segments, which means that they have more choice and flexibility in terms of where they shop and the entertainment opportunities available to them. This also has all sorts of other implications for marketers who need to be cognisant of the ability of consumers in this segment to transport goods, shop around and explore locations beyond traditional public transport routes.

Upper-middle class

The 'Upper-middle class' group comprises households earning R40 000–R75 000 per month. There are only 800 000 households in this segment, which is equivalent to around 4% of all South African households. This segment exposes the huge disparities in income inequality. With an average household income of over R60 000, the Upper-middle class account for nearly a quarter of all consumer spending power. Over half of this segment is white and nearly 70% of households include at least one adult who has a tertiary qualification.

The racial breakdown of this segment has shifted over the last decade and the proportion of Black African households has increased significantly. Marketers targeting this segment have to continually shift their focus and strategies to ensure they also appeal to new entrants in the segment.

Top end

'Top end' households earn over R75 000 per month and account for just over 1% of all South African households. In addition to income inequality, this group highlights the correlation between educational attainment and income. Nearly 80% of all Top end households include an adult who has at least an undergraduate degree. With an average household income of over R140 000, this segment accounts for around 14% of consumer spend. Over 60% of this segment is white and the most spoken language in the home is Afrikaans. Members of this segment often regard themselves as continually under time pressure. Indeed, a common desire is to eek out more time to pursue interests and commitments outside of work. As a result, they are likely to be receptive to products and services that offer a seamless experience and save time.

In the next section, these different segments are compared in order to help understand both inequality and the need for deeper thinking on development. If marketing's long-term goal is to provide for long-term societal needs (Chapter 1), then situational analysis is important.

Comparing segments

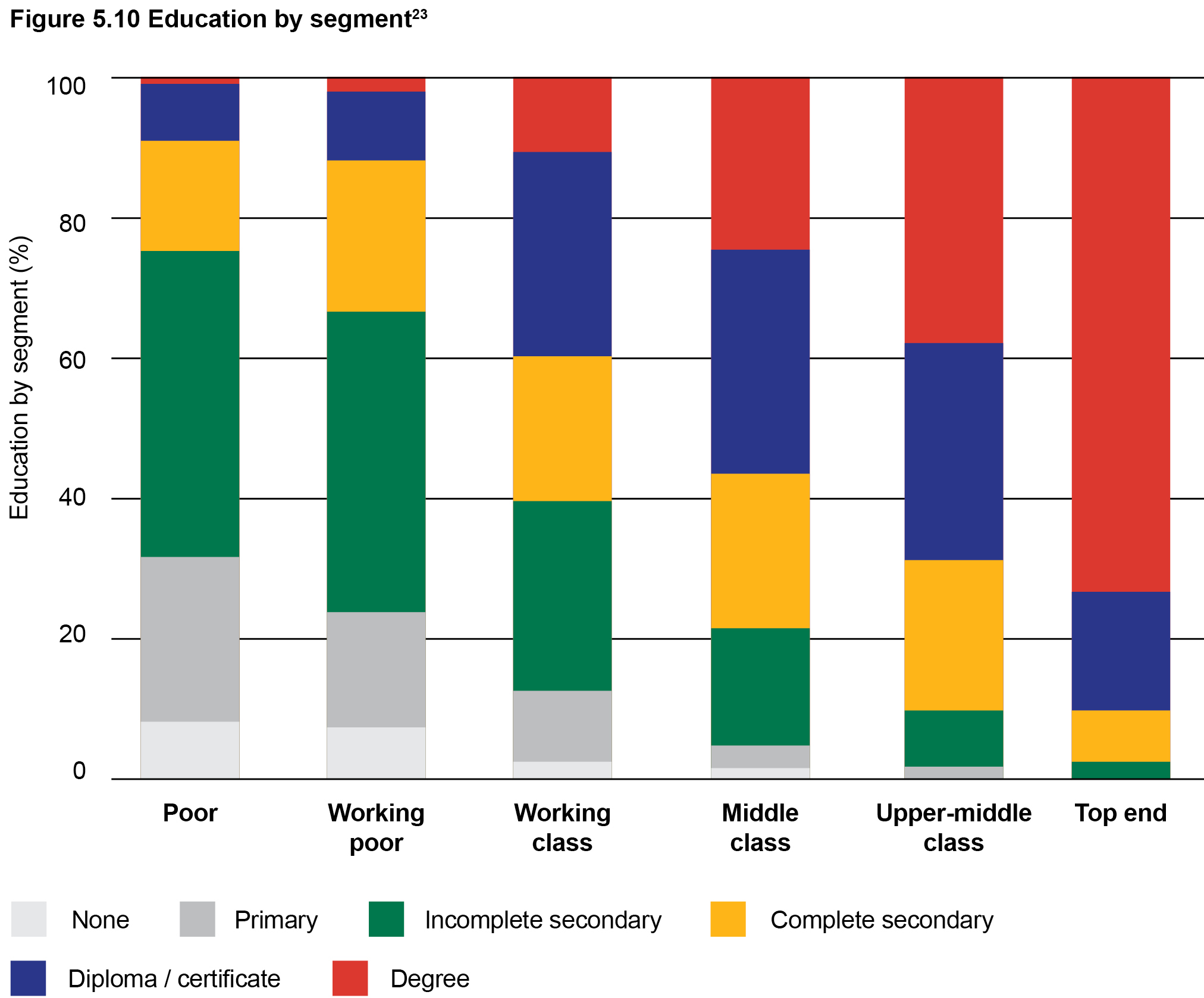

Each of the consumer segments described in the previous section is unique, but also forms part of a larger narrative around economic opportunities and outcomes. In addition, there is much income mobility between segments. Upward mobility between segments appears to be closely related to education. In Figure 5.10, it is clear that individuals in the Top end and Upper-middle class are much more likely to have a university degree than the poorer segments. On the other end of the spectrum, the majority of those in the Poor and Working poor segments have not completed high school.

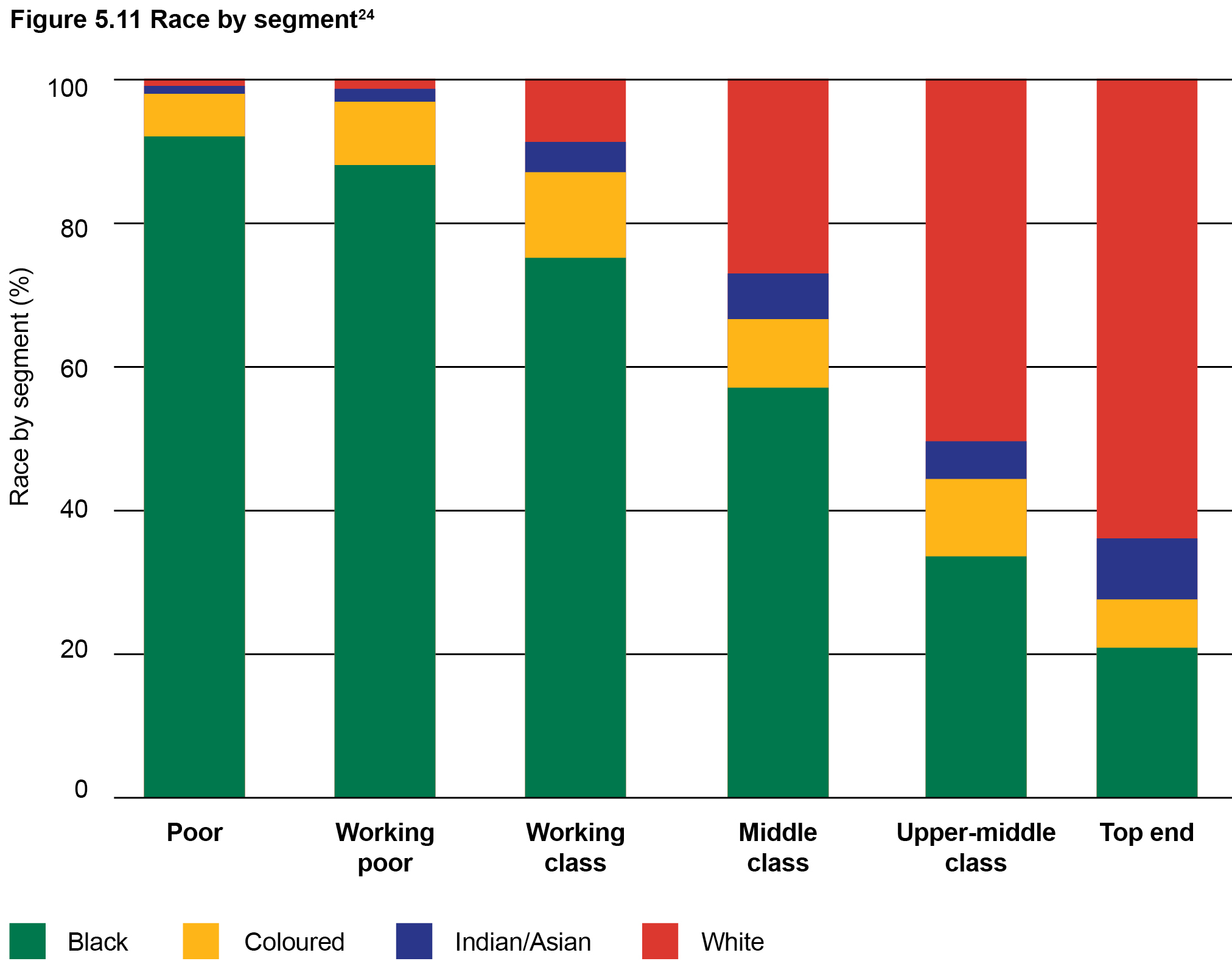

Similarly, economic outcomes are also closely related to race. Although the picture is continually changing and has moved significantly since the days of Apartheid, White households still dominate the wealthier segments such as the Upper-middle class and Top end (see Figure 5.11).

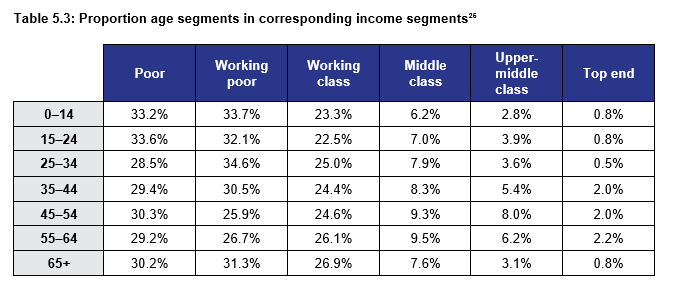

Table 5.3 shows the proportion of each of South Africa's age segments that fits into each income segment. Although the table contains a lot of information, the fact that most consumers in each age group are relatively poor is particularly relevant.

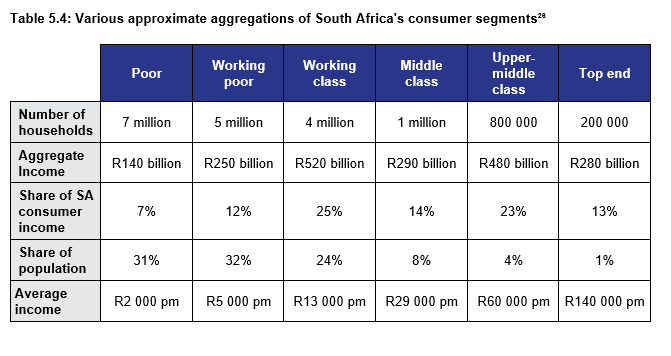

Finally, Table 5.4 provides an aggregated view of each segment by metrics that would be of interest to consumer marketers in South Africa. First, there is a breakdown of households per segment. Note that the Top end only has 200 000 households in South Africa. The row showing aggregate income for each segment shows the aggregate share of the country's overall consumer income. Finally, the segment's share of population and average income is reported.

The provided data show that South Africa's population is highly income mobile (both upwardly and downwardly). This means that these data will be highly variable over time. Nonetheless, consumer marketers should have a good grasp of these figures in order to understand the markets that they serve.

Conclusion

While there are many ways to segment consumers, this chapter provides a survey of South Africa's 60 million people in six major segments. This does not mean that people living in these segments are the same. They may live in similar economic circumstances, but they inevitably have different tastes, desires and behaviours. For marketers, understanding the consumer landscape is only one step when it comes to understanding consumer behaviour. Understanding differences within each segment and identifying needs and wants are just among some of the additional steps required if one is to truly connect with individuals in the various segments.