The South African Retail Landscape

Introduction

This chapter aims to provide an overview of South Africa's consumer goods retail environment and why it is so important for marketers to understand. The chapter looks at the formal and the informal retail sectors (both bricks-and-mortar and online) and the key role that each play in the market. The chapter is underpinned by the unique nature of South African retail, the history behind it, the forces that have shaped it, and the prevalent trends at play.

What is retail and why is it important for consumer marketers?

Every day, millions of consumers across the country visit retail stores, either physical ones (known as bricks-and-mortar stores) or digital ones, using the internet or cellular networks (e.g. USSD enabled transactions). They visit these stores to buy food and household goods (groceries), clothing, hardware, health and beauty products, and so the list goes on. Think about all the different types of stores you visit every week to buy the range of products that you need.

In formal terms, retail is defined as,

the activity of selling goods to the public, usually in small amounts, for their own use, including the resale (sale without transformation) of new and used goods and products to the general public for household use [1]

In the early days of the internet the line between 'pure-play'(Chapter 15) internet retail and bricks-and-mortar retail was much clearer. Today, most if not all major retailers trade across both, facilitated by continually improving IT systems and processes.

Retail is distinct from the business of wholesale, which is defined as:

an enterprise deriving 70% or more of its turnover from sales of goods to other businesses and institutions.

For example, a hair-care product such as a 'Black Like Me' hair conditioner purchased for a consumer's personal use is a retail sale, whereas a 'Black Like Me' hair conditioner purchased in bulk by a hairdresser to use in their beauty salon on a client's hair is a wholesale transaction. Both are product distribution and marketing channels, and both are important for consumer marketers to understand and engage with to achieve effective distribution and sales of their product to the end consumer. Marketers need to ensure that the right product variants and pack sizes are available in the right retail formats (whether physical or digital), at the right price, to appeal to the consumer who shops at that type of store (Chapter 15).

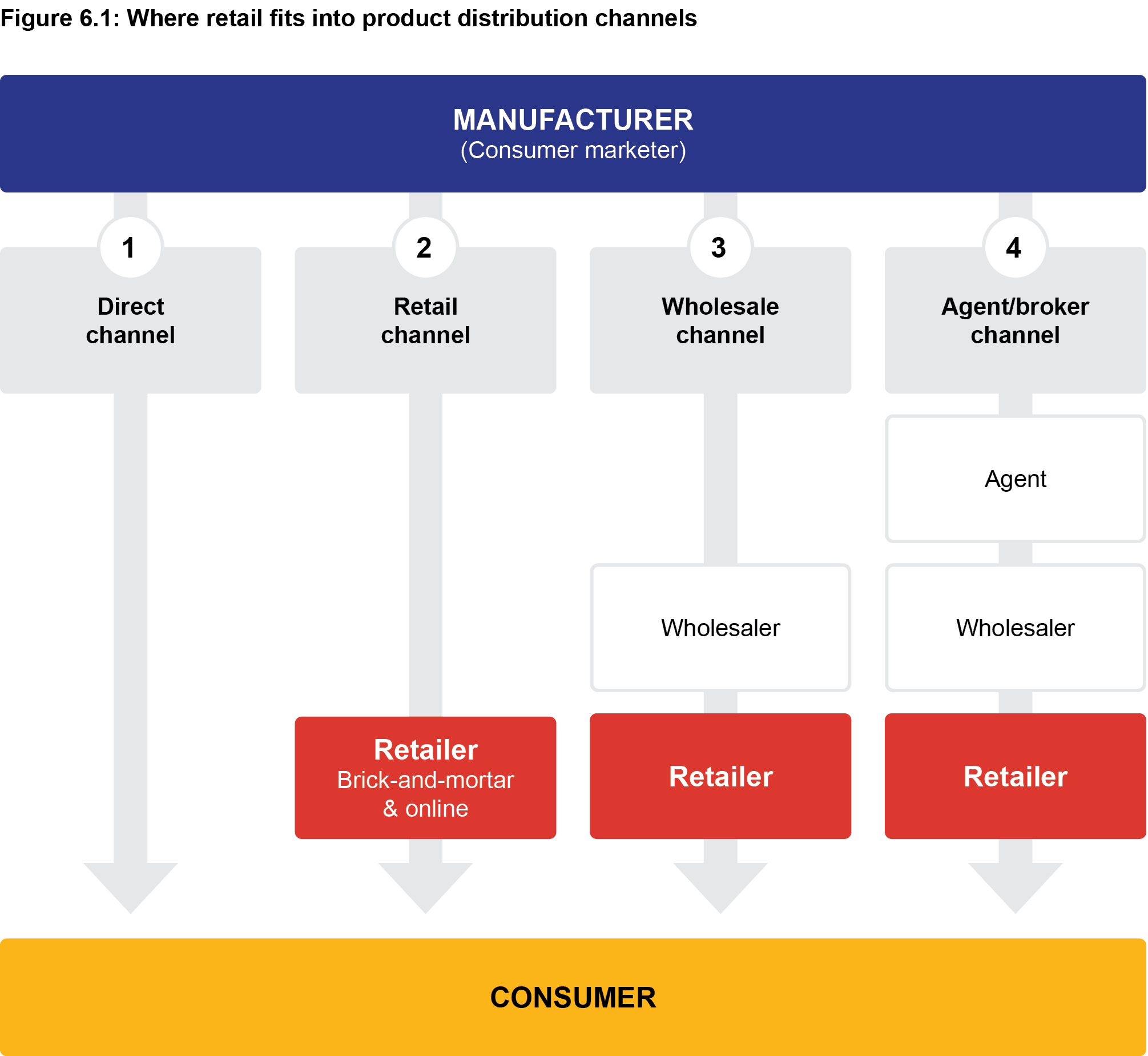

A manufacturer, unless selling directly to their end-consumer, needs to work with different networks of retail, wholesale, distributor and other organisations to bring their product to market. Figure 6.1 shows the primary distribution channels available to consumer goods manufacturers, but it is the retail channel that is most visible to the consumer. According to Mucuk, 'Retailers work as buying agents for consumers and as sales agents for their suppliers [2].

The retail store is the place where consumers are able to buy a wide range of different manufacturers' products in one place, from paint and garden equipment at Builder's Warehouse or Sizwe Paints to a fresh lettuce or cabbage at Makro or the spaza store down the road, to different types of speciality cheeses at Checkers or Pick n Pay. Figure 6.1. shows where retailers fit into product distribution networks. We explore the subject of product distribution channels and the role of these intermediary businesses in more depth in Chapter 15; however, because retailers have a direct influence on the manufacturer's product visibility, pricing, profitability and brand positioning in the market, it is very important for a marketer to understand the retail landscape in which they are working. In this chapter, we focus specifically on consumer goods (grocery) retail in South Africa.

The South African retail landscape

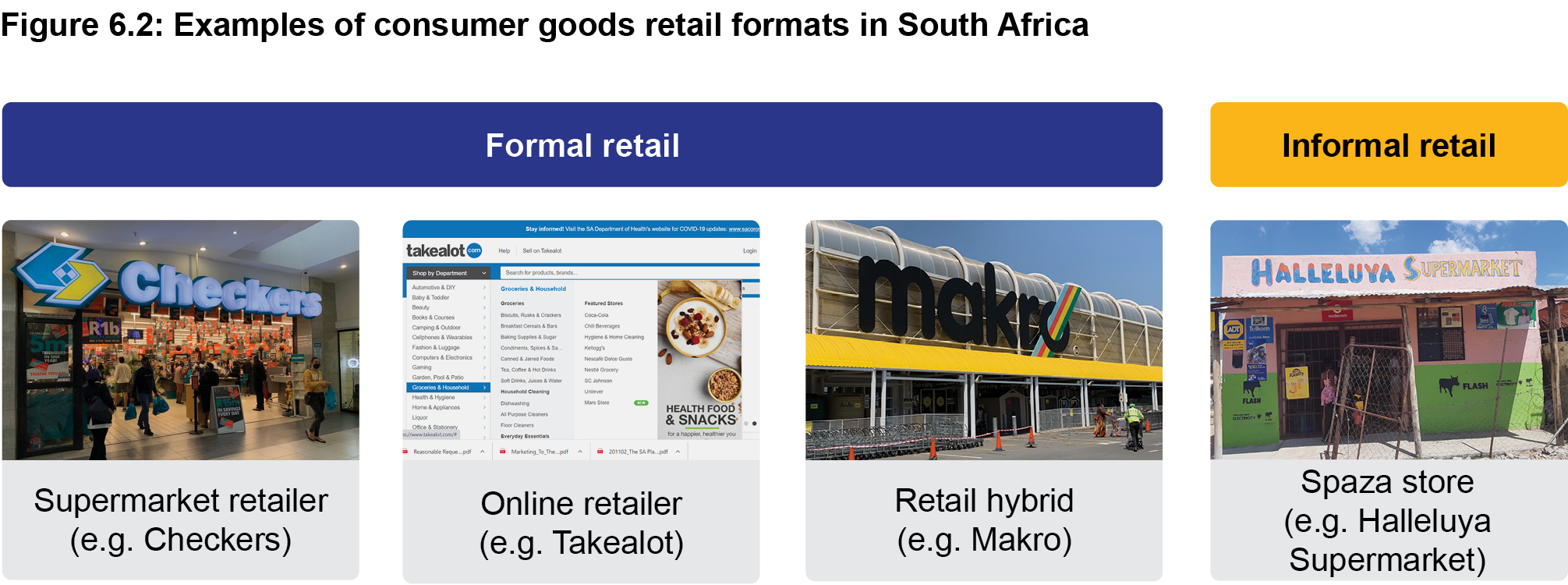

South Africa is a large, complex and dynamic country with almost 60 million diverse people of varying races, cultures and incomes, spread across nine provinces and speaking 11 official languages [3]. Vastly differing South African consumer needs and expectations along with unique political and socio-economic forces have resulted in a retail landscape that spans from sophisticated modern 'formal retail' chain stores, such as Woolworths, Checkers and Pick n Pay, largely serving upper-income consumers, to big-box cash-and-carry and hybrid stores such as Makro, to neighbourhood convenience stores like SPAR, to thousands of informal retail spaza shops selling food and grocery products in townships and poorer communities.

This mix of formal and informal retail businesses serves the cross-section of South African consumers; both play an integral role in the retail and consumer goods economy. Online retail can span both formal and informal retail operations. The differentiation between formal and informal retail is a natural place to start when looking at the different kinds of retailers in South Africa. It is also our first example of retailer classification, a process similar to consumer segmentation, but one which is done by marketers when selecting which retail channels to use to distribute their brand/product (Chapter 15).

The differentiation between formal and informal retail is important for a few reasons. The formality of a business and its ownership structure will affect how a manufacturer (consumer marketer) sells to and services the retailer and how much it costs to get their product onto that retailer's shop shelf. This cost is known as 'cost-to-serve'.

To be classified as a formal retail business,

a business must be operating within the official legal framework (of South Africa) and be registered with the South African Revenue Services, paying the relevant taxes on all generated incomes. [4]

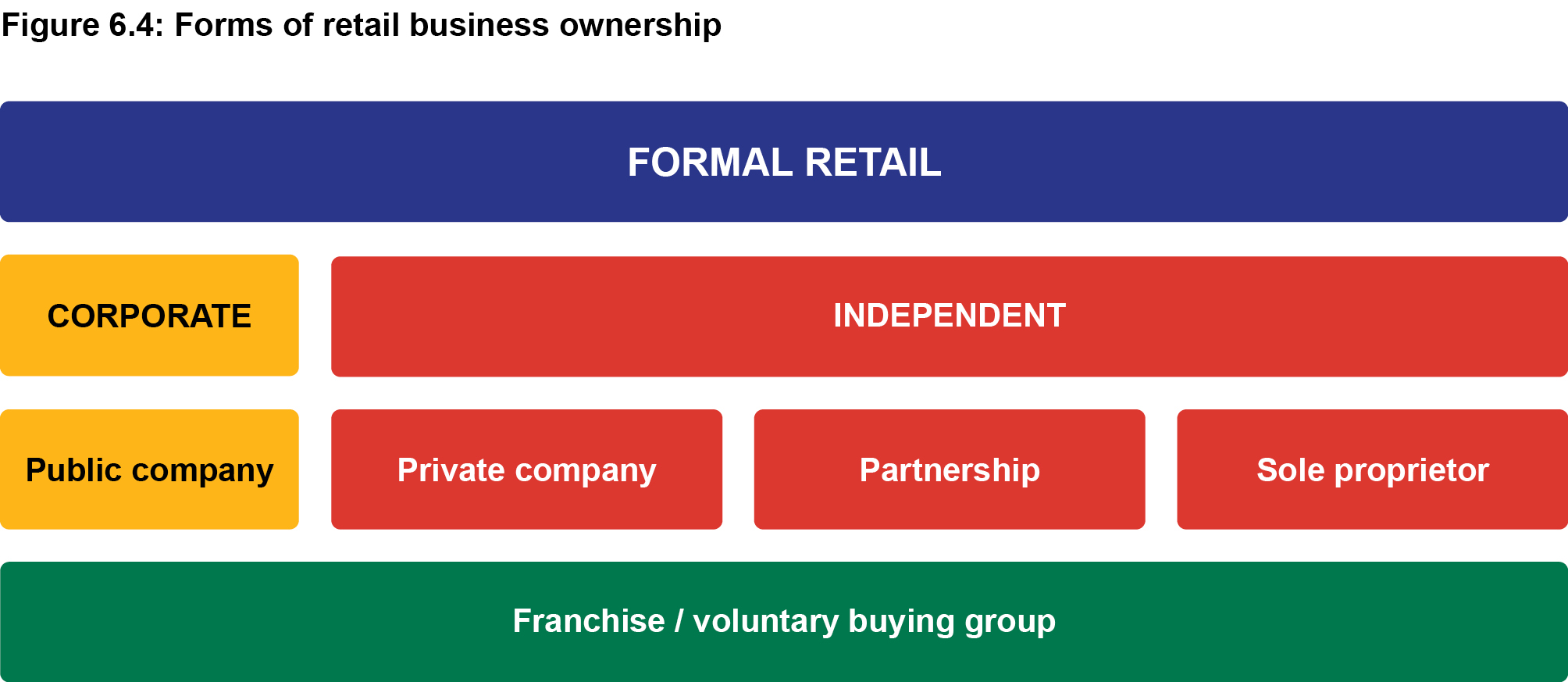

Within the formal retail sector, there are different types of retail business ownership structures ranging from corporate retailers listed on the JSE, such as the Shoprite Group and the Pick n Pay Group, to voluntary buying organisations such as SPAR and Unitrade Management Services (UMS) to small independent supermarkets operating as a sole proprietor. We look at formal definitions of these terms later in the chapter.

The definition of 'informal retail' varies across academic texts and between organisations, but essentially consists of small, unregistered businesses operating as street vendors and in-home businesses established on residential sites (often termed spaza shops or tuck shops in South Africa) [5].

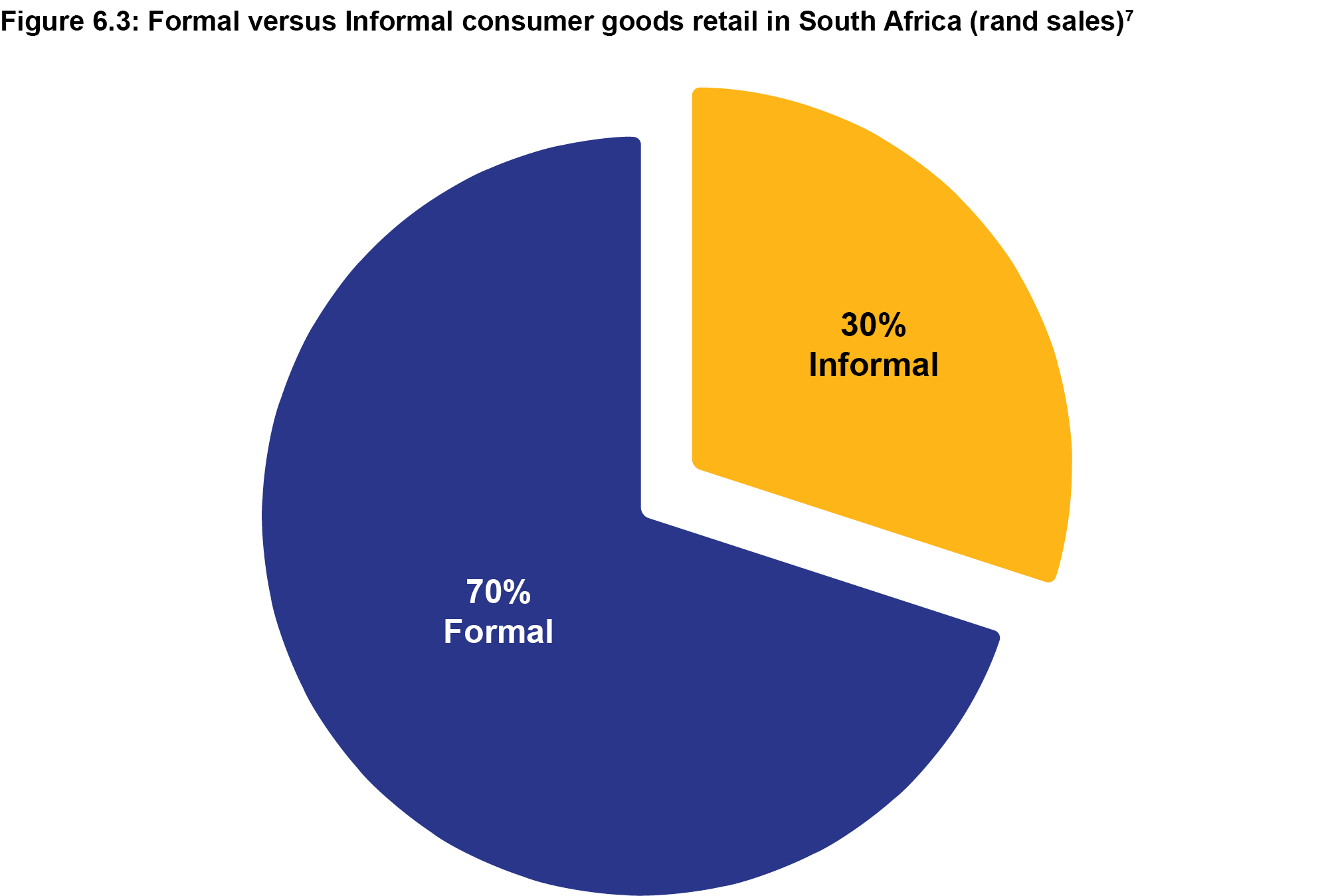

The informal economy in the South African retail context plays a vital role in employment, food security and income generation and it is an important contributor to business development. While the informal sector businesses usually lack formality in terms of business licences, VAT registration, operating permits and accounting procedures [6], these stores are not necessarily illegal operators. Trade Intelligence (Ti) reports that the relative size of the formal versus informal retail sectors is approximately 70:30, as shown in Figure 6.3. This 70:30 ratio will vary significantly depending on the manufacturer's product. Omo handwashing powder or White Star maize meal, for example, will have a far heavier informal retail sales weighting compared to basmati rice or olive oil, which would sell predominantly through formal retail stores to largely middle- to upper-income consumers.

Formal retail

The formal retail sector in South Africa can be, at its broadest level, categorised into corporate retail and independent retail. Within these classifications, there are different kinds of business-ownership models. This is important for marketers to take into consideration when working with their chosen retail channel partners (Chapter 15) because the business ownership model will impact and inform how the manufacturer engages and services that retailer. Examples of these are shown in Figure 6.4 and include public and private companies, franchises, voluntary buying groups, partnerships and sole proprietorships. Franchise and voluntary buying group structures can be corporate, listed businesses, such as SPAR and OK, or they can be independent, private companies, such as Unitrade Management Services (Pty) Ltd.

Forms of business ownership

The following are short definitions of some of the business ownership models prevalent in South African consumer goods retail:

- A limited liability company (Ltd) is a company established according to the Companies Act 71 of 2008. They can be either public or private companies.

- A public company is a business that is listed on the stock exchange and issued shares of company stock that may be bought and sold by the general The buyers of those shares become shareholders of the company and all shareholders have limited liability. The daily trading of the public company's stock by its shareholders determines the value of the business. All listed businesses are public companies but not all public companies are listed businesses. An example of a public company retailer is Shoprite Holdings.

- A private company (Pty Ltd) or proprietary limited company is treated as a separate legal The owners of a Pty Ltd are also known as the shareholders but shares are not publically traded. A private company must comply with a large number of legal requirements with financial statements needing to undergo annual auditing. An example of a private company retailer is Food Lover's Market.

- A partnership has two or more owners and a written partnership agreement. Partners will also pool their money towards a common goal, share specialised skills and resources and share in the ups and downs of business success.

- A sole proprietor is a business owned and managed by one person. It is the simplest form of business entity because the business is not separate from the owner.

- Franchise businesses and voluntary buying organisations are kinds of purchasing platforms which combine the needs of many independent businesses to secure lower prices. Whilst the franchise or buying group could be a public or private company, the franchisee or member is an independently owned business run as a private company, partnership or sole proprietor.

- A franchise is when a franchisor (the owner of a business) licenses their business to a third For example, OK Foods (Shoprite Holdings) licenses the rights to its name, operating procedures, branding, business expertise and other services to the franchisee, an independent retail business owner. The franchisee pays franchise fees and other agreed costs to the franchisor. When working with franchise retail organisations, manufacturers need to engage with the franchisor and the franchisees to make sure their product is well represented on the shop shelves.

- A voluntary buying group is a business that operates as a wholesaler to a group of independently owned businesses. These are smaller retailers who undertake to place a certain amount of their product orders through the voluntary group in return for better pricing and various back-up services (such as promotions).

Corporate Retail

The corporate retail sector consists of listed public companies such as Pick n Pay Stores Limited or Shoprite Holdings. The corporate retail sector is also sometimes referred to as modern trade, as stores generally have sophisticated fittings and fixtures, are part of a branded retail chain and have a formal supply-chain infrastructure. It is important to note that the term modern trade can be misleading as there are independent retail businesses which operate as modern trade retailers, Food Lover's Market being an example. A retail chain is where two or more retail outlets share common ownership, brand and standardised business practices.

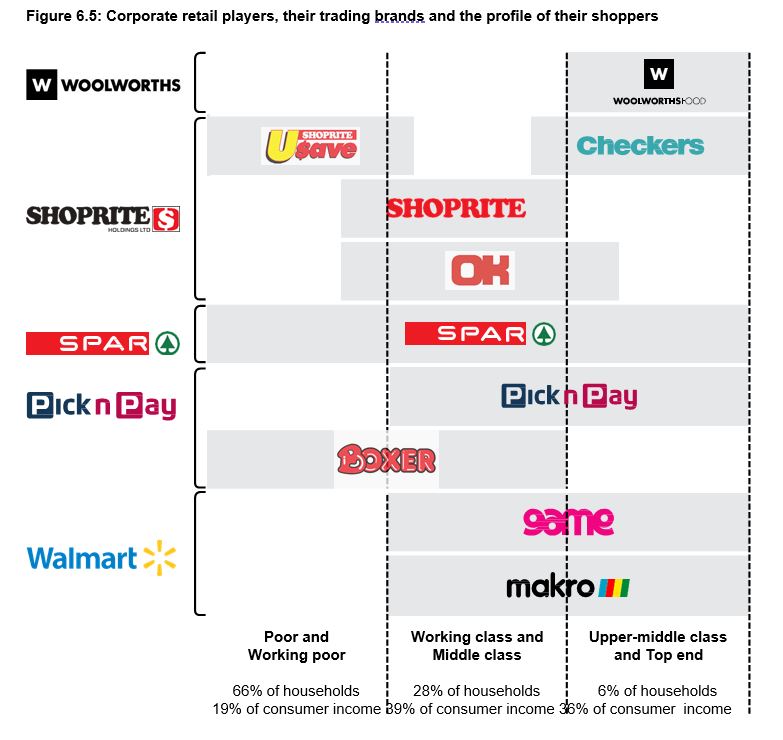

Corporate retail is dominated by five companies: Shoprite Holdings Ltd., Pick n Pay Stores Ltd., Massmart Holdings Ltd., (51% Walmart owned), The SPAR Group Ltd. and Woolworths Holdings Ltd., (Figure 6.5). In response to South Africa's high levels of income inequality, formal retailers have adapted with relevant formats and ranges to meet the needs of a shopper base which extends from the very poor to the extremely wealthy. Woolworths Food, Checkers and upper-income SPAR and Pick n Pay stores serve the wealthier segments with stores that can compete with the best in the world in terms of shopping experience and product range. Discounters and no-frills supermarkets, such as Shoprite, Boxer, Usave and Cambridge, bring mid- to lower-income shoppers quality food at low prices in a pleasant and clean shopping environment.

Figure 6.5 is indicative of how some of South Africa's corporate grocery retailer's serve the cross-section of South Africa's consumer's with their major trading brands. The profile of the shoppers has been segmented according to the National Income Dynamics Survey (NIDS) data [8].

Formal independent retail

Formal independent retail businesses range from a sole proprietor owning and managing a single store to a private company owning a chain of stores (Figure 6.4). The line between a voluntary trading organisation, buying group and franchise operation is dependent on how formal and how strict the terms of the contractual agreement between the member retailer and the principal company are. The principle company provides some or all of the following services to their franchisees or members:

- Centralised price and trading term negotiation with manufacturers

- Economies of scale achieved through collective buying

- Retail business skills support

- National or regional promotional programmes

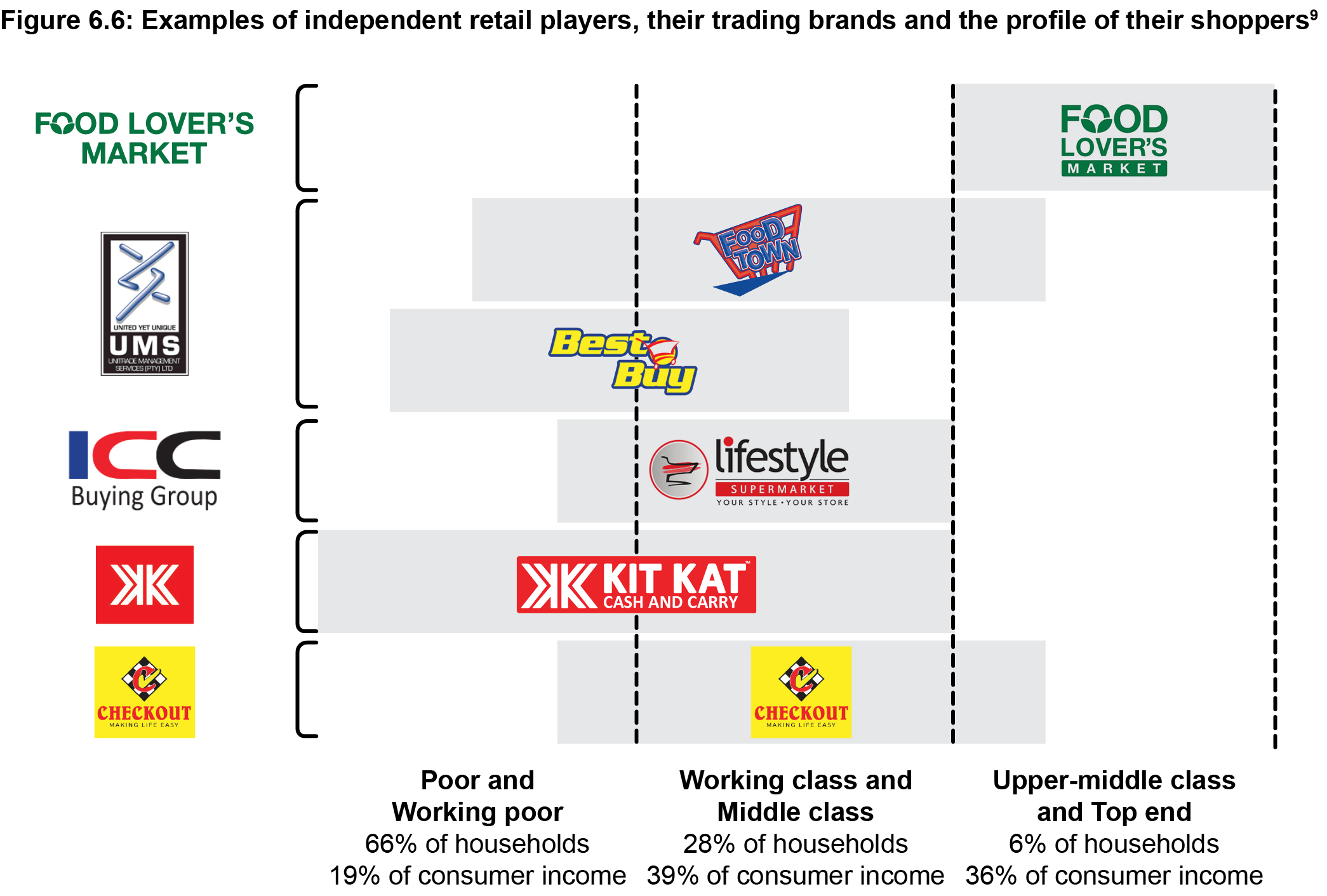

The independent retail sector in South Africa is characterised by strong regional independent chains such as Chamberlains (a hardware store focused in the Gauteng province) or Checkout (a supermarket chain trading in seven provinces) and small operators that may be operating independently or as a member of a franchise, buying group or voluntary trading organisation. Buying groups and voluntary trading organisations play an important role in this sector. Companies such as Unitrade Management Services (UMS), the Independent Buying Consortium (IBC), Shield (owned by Massmart Walmart) and the ICC Buying Group are largely unknown entities to the general public, as their business names bear no resemblance to their retail brands. For example, the ICC Buying Group's retail brand is Lifestyle Supermarket. Figure 6.6. shows some of South Africa's major formal independent retail businesses and the target consumers that shop in their stores.

South Africa's major buying groups, because of their historical membership profile (of predominantly wholesale cash-and-carry stores) are often classified as 'general trade' or as a part of the wholesale channel by consumer goods marketer's and are serviced as a wholesaler. This means manufacturers sometimes miss the product distribution and consumer marketing opportunities that these stores present. Examples of South African buying groups with retail and retail hybrid members are Unitrade Management Services (UMS), with Powertrade stores such as Powertrade Kuruman, Shield Buying and Distribution, with members such as Mambha Cash & Carry, and the Independent Cash & Carry Group (ICC Group) with its Lifestyle Supermarket stores. Corporate retailers who operate in the main market selling to lower-to middle-income consumers compete with these formal independent retail businesses (see Figure 6.7).

The shopping centre phenomenon in South Africa

South Africa has the sixth most shopping centres in the world, with over 2000 shopping centres spanning around 23 million square metres of formal retail space [10].

A shopping centre is,

a group of retail and other commercial establishments that is planned, developed, owned and managed as a single property, with on-site parking provided [11].

South Africa has a range of different kinds of shopping centres ranging from massive regional centres, such as the Mall of Africa in Gauteng or Gateway in kwaZulu-Natal, to relatively small neighbourhood and community shopping centres. Examples of these are shown in Table 6.1.

The acceleration of shopping centre development in the late 1990s and 2000s, including Maponya Mall in Soweto and Gateway Theatre of Shopping in Umhlanga, had a significant impact on the retail landscape. As well as serving the middle-to upper-income consumer in major cities, new centres provided corporate retail access into areas which they previously did not service and were largely the domain of informal retail and strong, regional independent retailers. In some cases, the pace of new shopping centre development put pressure on corporate retailers to open stores where they otherwise may not have; if they did not, another corporate retailer would.

There is a strong view that the rollout of shopping centres negatively impacted independent and informal retail. With shopping centre developers favouring major (corporate) retailers, it created a barrier to entry for strong regional independent retailers and significantly impacted South African spaza retailers. We explore this in more detail later in the chapter.

In recent years, a struggling Middle class, the consumer demand for convenient shopping solutions and online shopping have negatively impacted the number of consumer's visiting shopping centres, with many shopping centres looking at alternative ways to attract consumers, such as offering small craft markets on weekends or live entertainment.

Informal retail

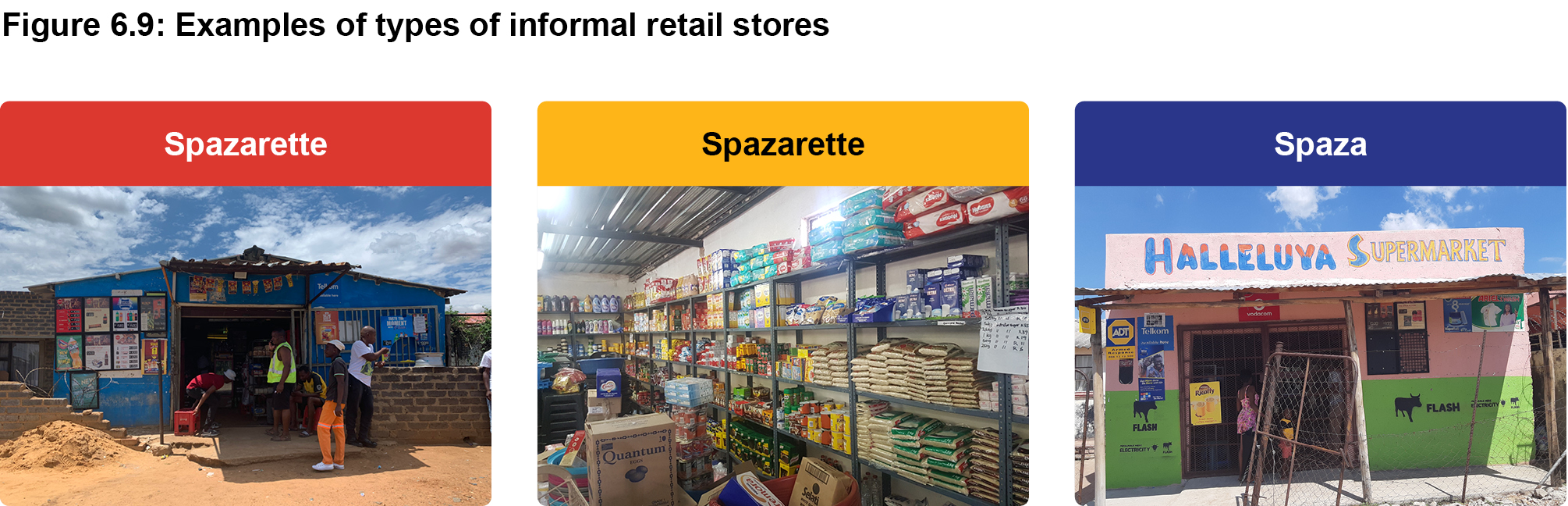

Informal grocery retail in South Africa ranges from hawkers and table-top operators to fixed structure, hole-in-the-wall stores, known as spaza stores, to small supermarkets referred to as spazarettes. In Chapter 15, we study the formal definitions of these terms. This chapter focuses only on fixed structure consumer goods retailers, but manfuacturers should not ignore hawkers and table-top operators or other 'informal' channels such as pharmacy (informal chemists), fast-foods and liquor (shebeen's), which are also important distributors of consumer goods such as confectionary (sweets and chocolates) and personal care products to township, rural and peri-urban areas.

The term spaza originated during Apartheid when trading restrictions were placed on Black people running businesses. It is not a direct translation of any South African language and there are different views regarding where the term originated, but in essence it means 'hidden', with stores hidden from authorities, trading from a roadside shack or from someone's bedroom window.

A spazarette store is larger than a spaza with a small supermarket-style offering (Chapter 15). Other terms sometimes used by manufacturers when referring to this sector of retail are General Trade (GT) or Traditional Trade (TT).

Few studies of the spaza trade at national scale have been made and the value of the sector differs depending on the chosen data source. Nielsen Holdings Plc (2016) have suggested that there are about 134 000 ‘traditional trade’ outlets, worth R46 billion in trade per annum, whilst Trade Intelligence (2020) value the informal retail sector at R158 billion [13].

Since the early 2000s the face of spaza shop owners has gone through significant change. We look at this evolution in more detail later in the chapter. It is estimated that 70%-85% of the approximately 100 000 spazarettes are run by immigrants, with four groups dominating – Somali, Ethiopian, Bangladeshi and Pakistani – with the first two being dominant in terms of numbers [14]. Many have permanent residency and hold a South African identity document, so are able to open a bank account, register for VAT and claim to pay tax. There are misconceptions about the spaza sector: that they are 'hole-in-the-wall', expensive, dirty and stock counterfeit brands. This may be true for some, but most spazas and spazarettes today offer relevant products in a convenient location, often with prices on par or cheaper than corporate retailers.

Informal retail operators can be grouped into two categories: [15]

- Survivalist

These are owner-operated spazas, mostly trading from the owner's home. These stores resemble the spaza stores of the 1980s and 1990s and are largely owned and run by South African traders. These businesses are informal because they have no choice.

- Networked

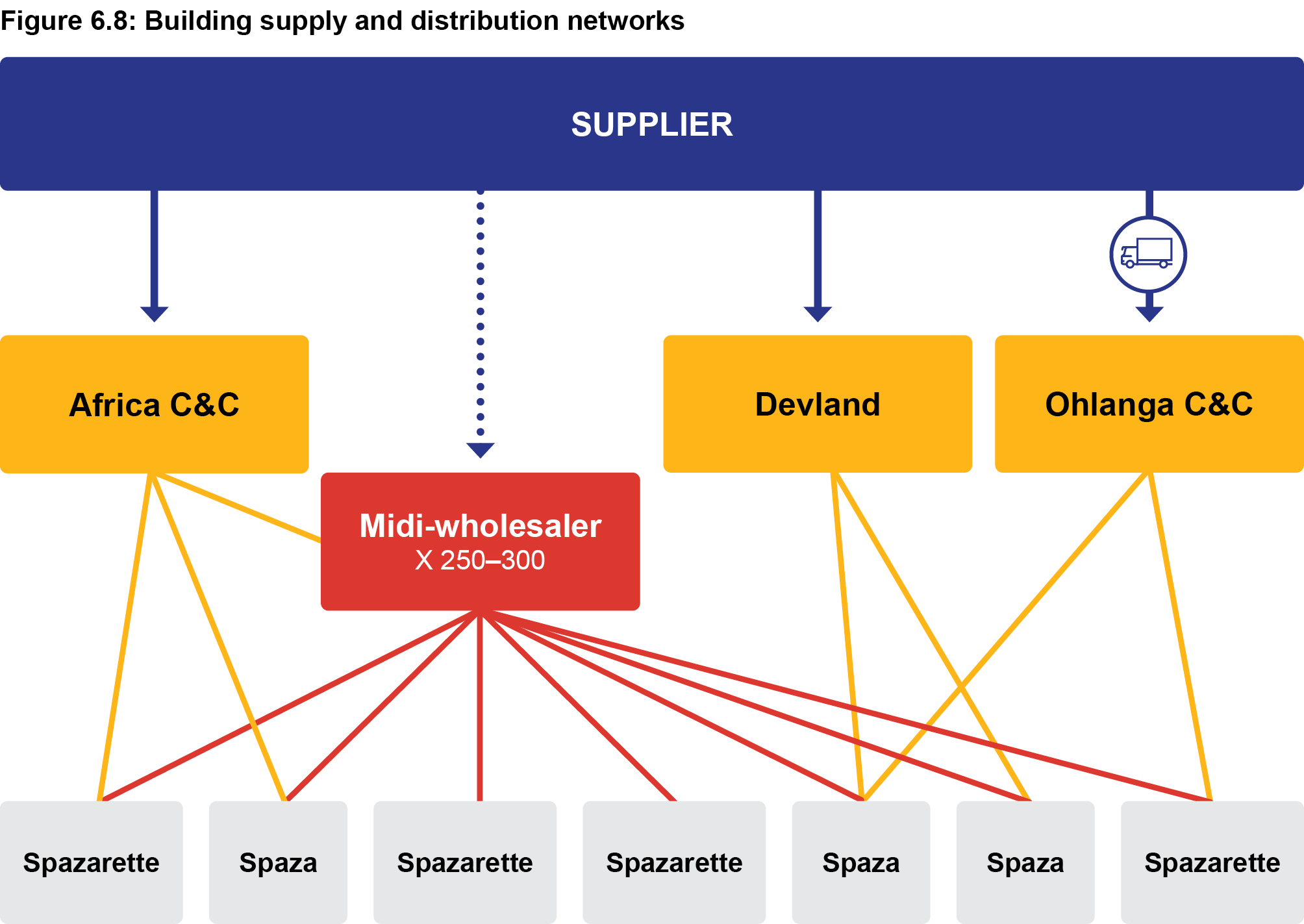

These are spazas and spazarettes that belong to a broader trader community network which facilitates more effective trading. Today, about one-third of spazas have evolved into spazarettes, most with brightly painted, branded store murals offering a clean, pleasant shopping environment to township consumers. The immigrant retailer community has grown to know South African township and poorer community needs and set up a network and informal collaborative trading infrastructure that has facilitated the growth of these stores into the significant players they are in the convenience distribution channel providing a viable alternative shopping destination for township and rural shoppers.A survey by marketing agency Minanawe, in conjunction with Standard Bank, in 2016, found that informal retailers were on average 7% cheaper than formal retailers on a basket of branded groceries. Adding transport costs to that saving, it gives consumers a strong incentive to shop at the local spaza or spazarette down the road. Within the Somali community, rather than being owner-operators, spaza store managers tend to work for those who own the larger upstream midi-wholesaler that supplies their stores with stock. Some of these upstream midi-wholesalers operate in networks with significant turnovers, sometimes travelling long distances to buy product at the best available price, whether it is from a large wholesaler, such as Devland or Ohlanga Cash & Carry or Shoprite or Boxer (Figure 6.8).

The definition of a midi-wholesaler is:

a small wholesaler which carries a narrow range of their spaza and spazarette customers' most popular product lines. They are located close to the spaza and spazarette customers they serve [16].

The outlets have remained largely hidden from manufacturers because they buy their stock from South African wholesalers (or retailers, depending on where they get the best bulk price). This is because most big brand manufacturers are not set up to transact with informal businesses such as these which predominantly trade in cash.

Challenges faced in measuring the informal retail market include the ongoing lack of official data, the frequent relocation of foreign immigrant spaza shopkeepers, the context of fear and violence and privacy concerns relating to the disclosure of personal income levels and shops' legal compliance.

Online retail

Ecommerce refers to commercial transactions conducted online. This means that whenever you buy and sell something using the internet, you are involved in ecommerce [17]. Ecommerce has transformed the process of buying and selling goods and its continued rapid growth is changing the nature of both business-to-business (B2B) and business-to-consumer (B2C) commerce, influencing product availability, inventory (stock holding), transportation patterns, pricing, and consumer behaviour worldwide.

For the purposes of this chapter, we will focus on a narrower definition of ecommerce known as e-retail (sometimes referred to as e-tail). E-retail is,

the sale of retail goods electronically via the internet [18].

Some definitions of e-retail exclude the sale of services, such as travel, eventing, accommodation and tourism [19].

Globally e-retail (or online retail) is unquestionably a growing force. Shopping online can make it easier and more convenient for consumers to purchase goods and services, eliminating the extra time and effort needed to visit a store and to be limited to shopping during regular shopping hours. However, despite predictions that it would lead to the end of bricks-and-mortar retail, across all product categories, pre-COVID total online retail sales only accounted for 1.4% of South African retail sales.

The growth of online retail (e-retail) in South Africa has been hindered by the following factors:

- Access and usage divide [20]

Of South Africa's population of nearly 60 million, 36 million belong to households earning R8 000 or less per month [21]. The high price of data and internet services creates an access divide across the population. The usage divide in the context of online retailing refers to those internet users who do not participate in online shopping. Of the approximately 28 million South Africans who have access to the internet, 21 million access the internet via their cellphones and only around 3.5 million engage in actual online shopping.

- Reliability and cost of delivery mechanisms

When data access and costs come down, delivery logistics improve and consumer trust grows, e-retail growth will accelerate [22]. Each of these levers are key for the growth of online retail, particularly in grocery's fresh and frozen food categories. The most popular online categories in South Africa include clothing, footwear, electronics and downloadable digital entertainment. In these categories online sales have put enormous pressure on bricks-and-mortar retailers. DionWired (owned by Massmart Walmart) is an example of an electronics retailer which had to close its doors in March 2020 as a result of competition from the likes of Takealot.

The category that has been the last frontier in terms of online sales growth has been fresh and dry (single unit) groceries. There is no app that can squeeze an avocado to check it is ripe. Until 2019, the only retailers that attempted to sell perishable (fresh and frozen) food online were Pick n Pay (launched in 2001) and Woolworths (launched in 2011).

This is largely due to how complex and costly it is to deliver small units of relatively low margin items to individual consumers. Providing a fresh offering requires a well-managed cold chain with refrigerated delivery vehicles or a short distance (travel time) between product picking and delivery point, with someone physically present to accept the delivery. This last stage of the delivery of the product into the hands of the consumer is known as 'the last mile'. For retailer's the term 'last mile' is defined as,

the end-stage logistics involved in getting orders to customers, as well as accepting returned goods [23].

In their efforts to grow sales and improve the profitability of online grocery sales, e-retailers have explored a range of last mile delivery solutions. We look at these trends in more depth later in the chapter and in the supply chain discussion in Chapter 15.

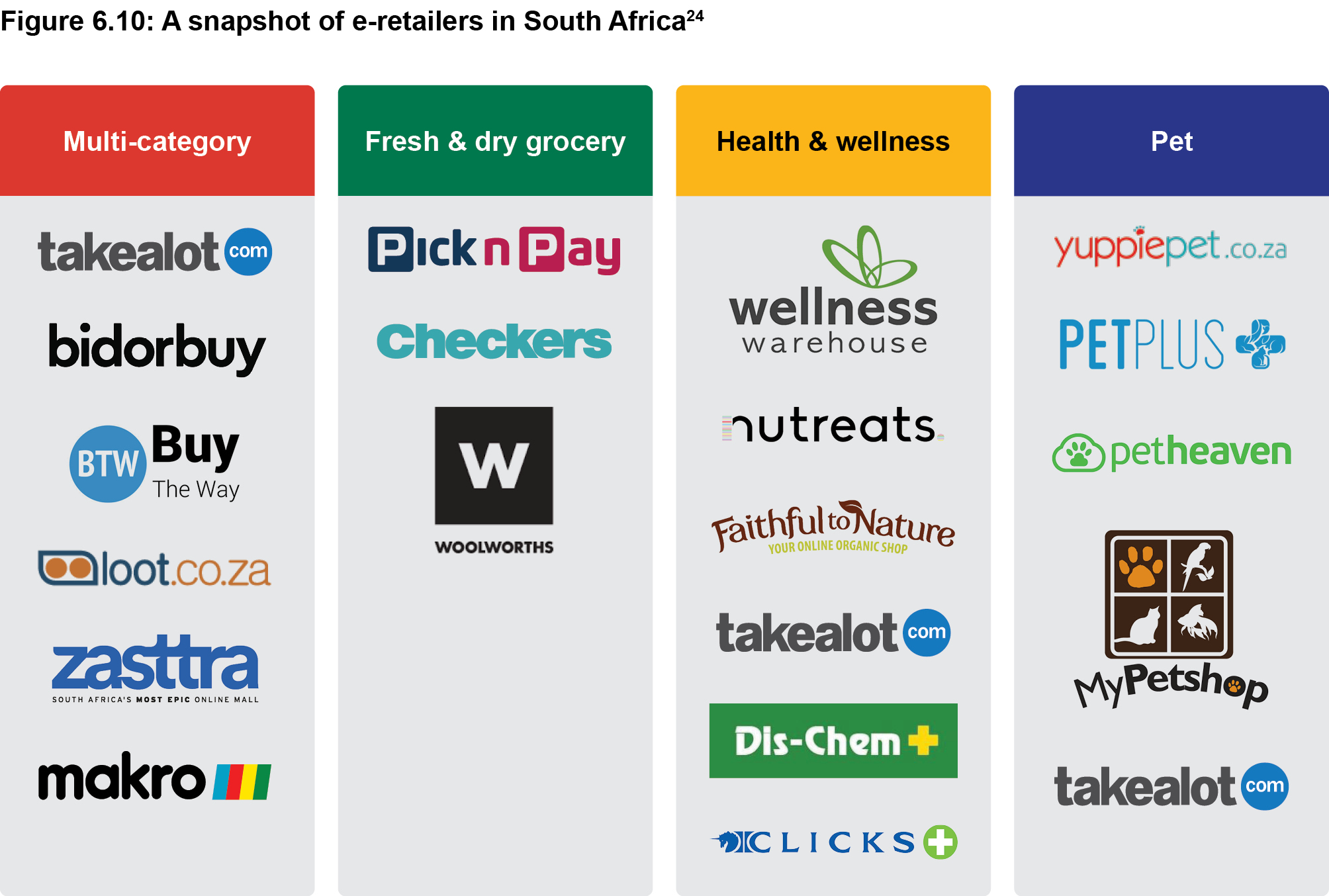

- Key online retailers in SA

There are two types of e-retailers in South Africa: pure-play e-retailers, such as Takealot. com: Zando.co.za and NetFlorist.co.za, and 'bricks-and-clicks' e-retailers such as Makro.co.za and Picknpay.co.za. We look at the definitions of these terms in more depth in Chapter 15. Figure 6.8 shows some of the e-retailers that sell consumer goods online. These range from multi-category retailers, such Takealot.com, bid-or-buy.co.za and Makro.co.za, to specialist e-retailers which focus on selling products in specific categories, such as pet care or health and wellness.

In the 'pure-play' arena, Takealot.com (established in 2011) is the largest e-retailer in South Africa and one of the largest on the African continent [25]. It trades across multiple categories, including electronics, lifestyle, media & gaming and fashion products. Since inception, Takealot has invested significantly in developing its logistics and distribution infrastructure.

In the (formal) bricks-and-clicks arena, retailers include Pick n Pay, Makro, Woolworths and Checkers. All offer home or selected drop-off point deliveries and click-and-collect services, where the consumer opts to collect the product in-store. Makro added conveniently located locker pick-up points as additional convenient solutions for their online shoppers. We explore these innovative solutions in more detail in Chapter 15.

The shaping of South Africa's retail landscape – looking back

The South African retail sector is an example of how significantly an industry can be shaped by a political context. In Chapter 1, we looked at consumer marketing in South Africa and explained the background to some of the consumer phenomena that were shaped by the South African consumer's context. Similarly, each of these phenomena had a fundamental impact on consumer goods retailing in South Africa. This section is divided into subsections Apartheid (1948—1994), democracy pre-financial crisis (1994—2008) and democracy post- financial crisis (2008—present) where we explain the impact of these phenomena on retailing and the retail landscape in the 2020s.

Retail landscape in South Africa during Apartheid (1948‒1994) [26]

During the Apartheid era of 1948 to 1994, the majority of SA's population endured an enforced process of segregation, with white people living, for the most part, in suburban enclaves and Black people being removed to high density townships or quasi-independent rural homelands. Townships were essentially sleeper suburbs for a cheap labour force, and as such had no commercial districts.

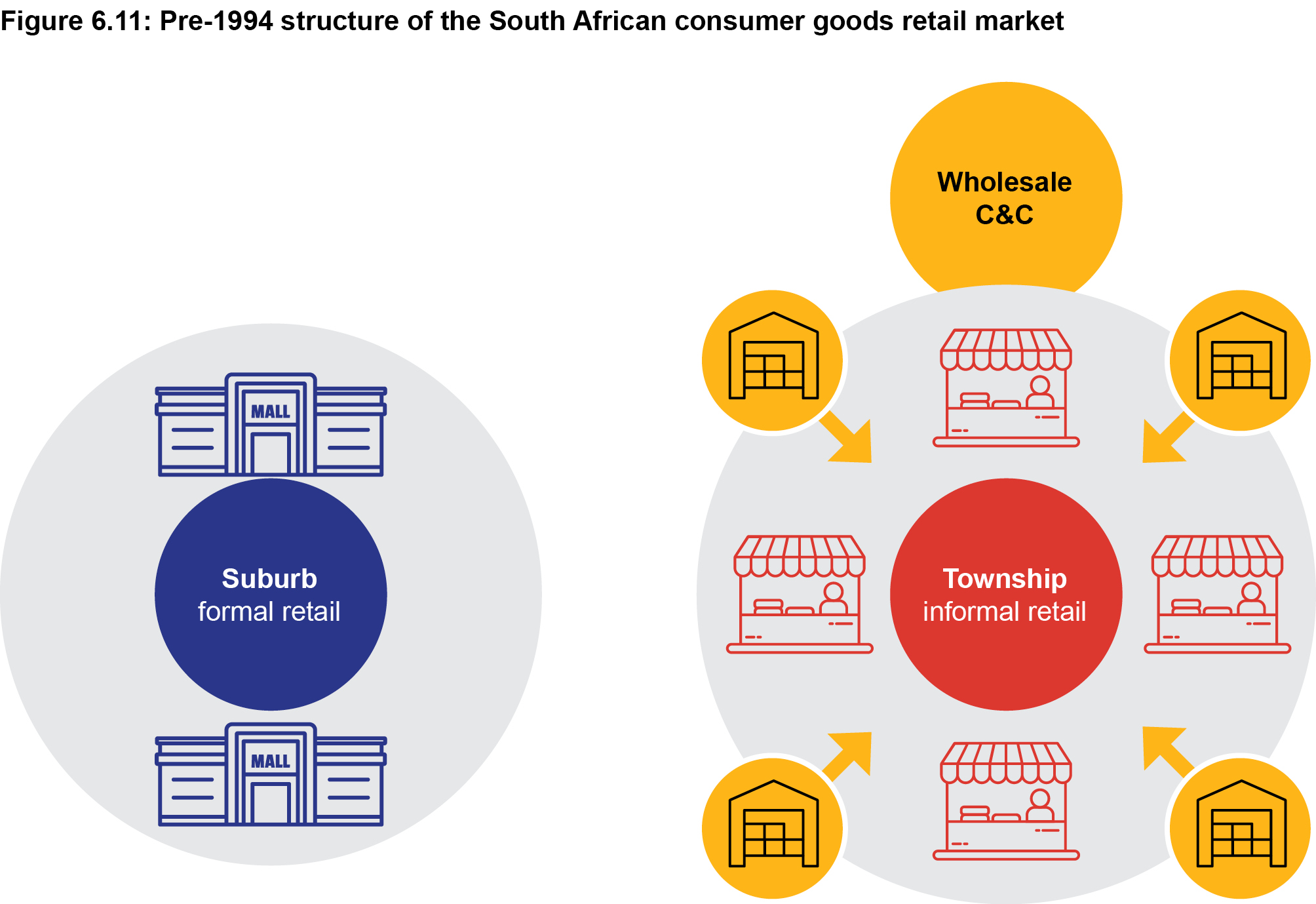

Corporate retailers such as Pick n Pay (founded in 1967) and Shoprite (established in 1979) focused on trading in major cities and upper income (white) suburbs. South Africa's Black consumers were served in homelands, smaller towns and outlying rural areas by licensed white-owned or Indian-owned shops, [27] such as KwaZulu Cash & Carry (later to become Boxer Cash & Carry, then Boxer Superstores) and SPAR member stores trading in places such as Empangeni, Nqutu and Mandeni, while township consumers were served by a vast class of township entrepreneurs running informal retail stores which became known as spaza stores. These South African owned spazas, which operated from the roadside or from a window in someone's home, carried a limited range of essential commodities and household products. They were generally more expensive than the formal supermarkets, but their location worked in their favour, saving township consumers money on transport costs.

To service these informal independent retailers, wholesale cash and carry stores such as corporate wholesale chain Metro Cash & Carry (no longer in existence) and independent wholesalers, such as Africa Cash & Carry and Kit Kat Cash & Carry, established themselves on the periphery of township areas and in commercial nodes to serve the thousands of spaza stores (Figure 6.11).

During this period consumers' shopping habits revolved around monthly bulk destination shopping at larger stores such as hypermarkets and supermarkets, with emergency top-ups and the 5 Cs (Cigarettes, Cellular, Cold Beverages, Confectionery and Chips) purchased during the week at smaller local supermarkets, corner cafés, garage forecourt retail shops or township spazas.

Retail landscape in South Africa post-Apartheid (1994‒2008)

Between 1994 and 2008, the lifting of trading restrictions resulted in significant shifts in the retail landscape. Two main phenomena occurred. First, corporate retailers such as Shoprite and Pick n Pay identified the significant untapped township market and moved into the townships, key commuter nodes and former homelands. Second, regional malls opened in most major townships (for example, Maponya Mall in Soweto and Umlazi Megacity in Umlazi, south of Durban). The resulting impact on informal retail in the townships was significant. Unable to compete with these supermarket chains, the South African owned spaza stores either went out of business or shifted their focus to sub-leasing their premises. Another factor that hit informal retail hard was the shift in 2005 of social grant pay points from cash pension days in communities to SASSA pay points at corporate retailers such as Shoprite and Boxer. This shifted significant amounts of money out of the township communities into the formal retail sector.

The knock-on impact on wholesale cash and carry businesses led some to believe that the wholesale channel was under serious threat of disappearing. Some manufacturers withdrew their investment from wholesale and informal retail, redirecting their trade spend to formal corporate retail. At the time corporate retailers were regarded as easier and more cost-effective to service and they were rapidly providing alternative means of selling to low income, main market consumers. It was during this time that the first wave of consolidation of the wholesale channel took place. A number of medium to large independent wholesale businesses banded together to establish buying groups to improve their buying power in an attempt to compete with the major corporate chains. The Buying Exchange Company (Pty) Ltd was established in 1999 as a buying support group for both independent retailers and wholesalers [28]. Similarly, Unitrade Management Services (UMS), Independent Buying Consortium (IBC) and the Independent Cash and Carry (ICC) Group were established in 2001, followed later by Tradeport Distribution (Pty) Ltd (2003) and Elite Star Trading Africa (EST) (2007). The demise of Metcash, South Africa's biggest corporate wholesale business with its Metro and Trade Centre wholesale chains in the 2000s can, in part, be put down to the evolution and consolidation of the independent wholesalers and the near demise of township spazas.

The real boom for growth in formal consumer goods retail came post-2001, with major GDP growth and the continued rise of a new Black Middle class. Consumer demand for convenience accelerated during this time and shopping habits began to shift from monthly 'big shops' to daily and weekly shopping. For corporate retailers it was a time when just selling food and groceries was no longer enough and growth could no longer only come from new stores (there were over 300 new store openings across corporate retailers in 2006 alone). Corporate retailer began a race to differentiate from one another using various means including offering a growing range of lifestyle services, such as Shoprite Group's Money Market offering and home meal replacement counters, to focusing on building the equity of their brands. From retail to wholesale, PnP to SPAR, Shoprite to Boxer, retailers focused on their brand identity, each striving to establish that brand as the most desirable to a shopper who has an increasing number of choice shopping destinations. For South African middle- to upper-income consumers, this meant access to world-class retail offerings at a rapidly increasing number of conveniently located stores.

The forecourt retail convenience channel transformed in the ten years from 2000, with partnerships established between petroleum companies and corporate retailers. This transformed the face of forecourt retail convenience stores. Woolworths Foodstop at Engen garages opened in 2000, the first Pick n Pay Express store at BP in 2008 and, in 2009, FreshStop at Caltex, a partnership between Fruit & Veg City and Chevron SA [29].

By the end of this period, most of the corporate retailers in South African had expanded into new markets beyond South Africa's borders across Africa, where rapidly expanding economies were demanding retail solutions to match their aspirations. They had also expanded into new retail formats outside of their core grocery offerings, opening liquor stores such as Tops at SPAR, DIY stores such as SPAR Build-it and pharmacy outlets, such as MediRite. The Shoprite Group illustration (Figure 6.12) shows the number of trading brands that this retail group offers consumers. Within their grocery portfolio the group uses different brands to target different consumer segments. For example, Checkers is positioned as the upper-income supermarket brand targeting the upper income consumer and Shoprite is the main market supermarket brand targeting the lower- to middle-income shopper (see Chapter 11 and 12 for a discussion on segmentation and positioning by using different brands).

Online retail emerged in South Africa in 1996. Kalahari.com, which was to become one of the biggest players in the early 2000s, was launched in 1998 [30]. Over this time, because of the relatively low barriers to entry, the market saw a number of online retailers enter the market. Many of these focused on specific categories, operating as specialist e-retailers (see Figure 6.10) and many have remained relatively small in terms of traffic

Retail landscape in South Africa post financial crisis (2008‒ present)

When the global financial crisis hit in late 2008 it had a major effect on consumer confidence, particularly when it became apparent that South Africa, despite a sound banking sector, was not immune from the fallout. The South African economy has bucked the global trend since the great recession of 2008 by remaining stagnant while the world recovered its economic momentum pre-COVID. Gross Domestic Product (GDP) growth fell below 1% in 2019 and the economy dipped in and out of recession [31].

The current retail reality is no longer a case of 'managing through tough times'; these tough times are the new normal. The question is how to thrive in this economic reality of low growth, high competition and significant pace of technological change. The competition for every shopper at every shopping occasion is intense and retail businesses have had no choice but to evolve in response, bringing a greater focus on the (product) mix in store and on disciplines within retail businesses and in the supply chain. Making a profit as a consumer goods retailer or wholesaler today is more challenging than ever.

In the following two sections, we discuss some of the trends that are evident in formal retail (including online) and in informal retail:

Formal retail

- Channel blurring

In a tough trading environment, businesses will look up and down the value chain for opportunities to increase their sales and profit margins. This means that lines between the distribution channels can become blurred (Chapter 15). Wholesale cash and carry stores have extended their retail offering to attract consumers; large wholesalers have established their own franchise retail chains and corporates like Pick n Pay are operating some of their hypermarkets as wholesale outlets selling to smaller independent retailers. This channel blurring has been a feature of the South African retail marketplace for the past 20 years.

- Best price and what it takes to get there

More than ever, product selling price is a primary determinant of where consumers will shop for food and groceries. For a retailer to sell at the best price it can, while still running the business at a profit, it needs to have the buying power to negotiate with manufacturers and it needs to run efficient business operations (in other words, manage its costs). The success of the discounter retail model (Chapter 15) has seen a number of full range supermarkets begin to reduce the number of product lines they carry. The more product lines a retailer stocks, the more complex it is for the retailer to manage its stock. Boxer led the way, shifting from a supermarket to a soft-discounter model and cutting the number of product lines from around 15 000 to 1 500—2 000. The impact this has on trading efficiency and ability to keep operational costs down is significant.

Private label is another means by which formal retailers (both corporate and independent) achieve better selling prices and, in most cases, better profit margins. With the strength of many South African retailer's brand equity, consumer's trust in these brands means that formal retailers' private label products have become an increasing threat to brand manufacturers.

The biggest recent development on the retail calendar is Black Friday which has shifted the centre of gravity for retail from December festive season trading to late November (now sometimes lasting the whole of November) in both online and bricks-and-mortar retail, To compete for a share of the consumers wallet, manufacturer's and retailers now need to have a Black Friday strategy.

- Margin through efficiencies and environmentally sustainable solutions

With increasing pressure from consumers and the impact that sustainability initiatives can have on efficiency and cost saving, there has been a realisation that integrated sustainability is a critical conversation and an important route to margin. Sustainable power supplies and smaller carbon footprints, for example, have transitioned from being nice to have to an essential part of doing business.

- Growth in convenience retailing and value-added service offerings

In broad terms, convenience retailing is not just about the size of the store and the range of products it carries. It includes those things that retailers do to meet the consumer's ongoing demand for convenient shopping solutions. It has led to significant innovations among consumer goods retailers over many years. Some of these convenience-driven trends are:

- Value added services

Value-added services (VAS) became a focus across food and grocery retailers in the 2000s. This trend accelerated when the Shoprite Group acquired Computicket in 1995. The growth in VAS was driven by the consumer's demand for convenience and by the retailers' race to differentiate from each other, striving to be the consumer's shopping destination of choice. By 2015, money-transfer VAS such as cash withdrawals, payment of utility bills and buying airtime at your local (formal) retailer were the norm. The trend continues as retailers expand their lifestyle services whether it is in healthcare, nutrition, beauty advisory services, parenting support, hospitality or banking.

- Cashless transactions / payment solutions

The acceleration in cybercash (cashless payment) solutions range from the mobile payment technology and digital payment apps offered by Woolworths to those used by informal traders, such as iKhokha. At formal retailers, the acceptance of card payments has been the norm for decades. However, in poorer communities cash has remained king despite many attempts by businesses to promote cashless payment solutions to informal retailers. COVID-19 saw the acceleration of online and alternative payment solutions in the marketplace. An example is Shoprite's virtual grocery voucher service launched in April 2020. Within an hour a grocery voucher can be sent to a recipient's cellphone [32]. This type of grocery voucher solution presents the government and businesses with the opportunity to distribute food parcel funds in a secure way for example. The question is whether 'pushing public funds into a food voucher system redeemable only at corporate supermarkets only aggravates economic exclusion as it forces people to spend their money at (corporate) supermarkets bypassing informal traders, further pushing poor people out of economic activity' [33].

- Growth of consumer goods e-retail with innovation in last mile delivery mechanisms

The year 2011 saw the launch of Takealot, which, along with Kalahari and Bid-or-Buy, became the biggest multi-category e-retailers in the South African market. The 2014 acquisition of Mr Delivery, South Africa's largest restaurant food delivery service, gave Takealot ownership over its own logistics network and resulted in their on-demand food delivery service. Although still small, it means Takealot began to compete with South Africa's major bricks-and-mortar grocery retailers.

The first food and grocery retailers to launch online grocery shopping (including fresh and frozen goods) were Woolworths with IntheBag in 2000 and Pick n Pay which launched online in 2011. In 2014, Naspers-owned Kalahari.com and Takealot (including the newly acquired Superbalist) merged and in 2018 Naspers upped its ownership in Takealot to 96%.44 Its significant shareholding in Chinese giant Tencent, first acquired in 2001, gives it access to cutting edge online retail strategic thinking.

Major factors in the growth of e-retailing are logistics capabilities (getting the product into the hands of the consumer at their home or workplace) and technology capabilities (the digital capability to do it). We look at these in more detail in Chapter 15, but the note to make here is that innovation and development in logistics infrastructure and last mile delivery solutions with services such as pargo.co.za's click and collect and product returns solution for retailers and manufacturers and delivery solutions such as Checkers Sixty60 and eButler will mean accelerated growth in consumer goods e-retailing across formal and informal retail businesses.Technology literacy, data quality and accuracy (of both product master data and inventory data) and the right systems architecture are key to effective delivery of online retail.

- Growth in online subscription models and mealkit solutions

Subscriptions services are growing in popularity in categories such as health supplements, dog food and high value personal care items, such as razor blades. Categories with regular cyclical orders and where consumers tend to stick to one brand are excellent targets for the subscription sales model. The risk for consumer goods retailers is that products where they make higher margin, such as razor blades, could fall out of the bricks-and-mortar retail basket as subscription services grow.

Mealkit solutions are another growth area on online convenience retail. This too is a threat to supermarkets as it is the high margin goods, such as fresh produce, deli, buthery and bakery lines which are included in the UCook mealkit offering

- Continued challenge of data management and insight generation

The digitisation wave over the past 20 years means higher and higher volumes of data are being shared, captured and stored. Consumer buying patterns and habits produce data which inform decision-making across the grocery channels and the retail players, from Shoprite and Makro to Jumbo, Tradeport and other formal independent retail operators. Many formal retailers have their own data departments as well as employing third-party data analytical services to assist with turning the volumes of available data into meaningful business decision-making tools. An example of an area where data management and reporting are very important is in the management of the product ranges that the retailer carries in stores.

A Boxer or Shoprite in Khayelitsha cannot carry the same product lines as a Shoprite or Boxer in Nqutu. They might both be stores that sell to lower-income consumers, but the demographic and brand preferences of their consumers are different. It is the point-of-sale data that will tell the retailer and the supplier which stores should carry which products, variants or pack sizes (Chapter 15).

Informal retail

- Providing healthy competition to corporate retail but with xenophobic challenges

Most South African owned spaza stores did not survive the onslaught of corporate retailers into townships and commuter nodes. However, as discussed earlier in the chapter, from around 2009/10 a new shape of spaza store took shape, with the entry of immigrant retailers.

The result has been a resurgence of informal retail as these immigrant-run spaza stores compete with the corporate retailers on the selling prices of products, providing a viable alternative shopping destination for township and rural shoppers. In the last decade, the growing realisation of the importance of the informal retail sector for product distribution to manufacturer's has led to greater efforts to access this market, measure it, gather data from it and sell products to it. Xenophobic violence is an ongoing threat to immigrant retailers, whether they are operating legally or illegally, often because of the belief (and in many cases,misconception) that they have taken business and jobs from South African's. This is a contentious issue which impacts the stability of the grocery retail sector and township communities.

- Cashless Payment solutions

The number of South Africans with access to formal banking products has grown significantly through the likes of Capitec, Thyme Bank and distribution of SASSA cards, but the number of card acceptance locations, especially in rural and peri-urban areas, has not grown in tandem.45 Since around 2014, there have been a number of efforts to provide cashless payment solutions for spazas and spazarettes. Pre-paid services terminals and voucher services such as Kazang, Flash and Blue Label Telecoms are accelerating the scope and scale of value added services (VAS) that informal retailers can offer, however this has not yet evolved to acceptance of card payments or cash withdrawals.

Conclusion

This chapter provided an overview of the consumer goods retail landscape in South Africa. We looked at the formal sector across bricks-and-mortar, online and omnichannel retail and the informal retail sector and the key role that each play in the market. The chapter was underpinned by the unique nature of the South African retail market, the history behind it, the forces that have shaped it and some of the prevalent trends at play.

Acknowledgements

The author would like to thank the following people for their expertise and willingness to contribute to channel relevant content:

Colin Fleming and Craig Risi for their contribution to the online retail section of the chapter GG.Alcock for his review of the informal retail channel and the team at Trade Intelligence for the use of material developed during the author's tenure as Managing Director.