The South African Media Landscape

Introduction

In this chapter, we explore the media landscape of South Africa. Consumers are constantly consuming media in various forms. Whether watching a movie on Netflix, reading a copy of the Soccer Laduma newspaper, seeing an Instagram post or listing to Umhlobo Wenene FM radio, we experience multiple forms of media all the time. Media are a crucial component of consumer marketing because most marketing communication is delivered through some form of media platform. As a marketer, understanding the basics of media planning can help to create a competitive advantage and reduce wasted advertising expenditure.

While there is some fairly complicated terminology in this chapter, this overview will help equip you with a basic understanding of media and media planning in South Africa. Below are a few key definitions when discussing media, which will be helpful in reading this chapter:

Audience [1] is the total number of reported individuals who are exposed to any given media platform, often referred to as listenership (radio), viewership (television) or readership (newspapers and magazines) and usually forms the basis for the pricing of advertisements sold by commercial media.

Media reach [2] refers to the number of households or people within your target market, who are exposed to the advertising message at least once. This is usually reflected as a percentage and is often referred to as coverage or cover.

Media frequency [3]is the number of times, on average, that a person within the target market is supposed to have been exposed to the advertiser's message.

Media planning [4] refers to a specific and detailed process of reaching the right number of appropriate people (reach), the right number of times (frequency), in the right environment at minimum cost, to achieve the brand's marketing objectives.

Media planning: Content, channels, context and consumers

The primary objective of successful advertising is not creative expression and aesthetic appeal as an end in itself, but rather the contribution to powerfully persuasive and commercially rewarding communication. Creativity awards may remain highly prized decorations on the walls of advertising agencies from Madison Avenue to Sandton, but the real contribution of creative advertising is increasingly being measured in the marketplace.

In order to maximise the effectiveness of any commercial communication, we need to take cognisance of, not only the advertising content (the message), but also the channel (the medium) and the context through which that content is delivered to consumers. It is this last perspective which underpins the advertising discipline of media planning.

The World Federation of Advertisers [5] (WFA) Media Charter defines the term 'medium' as:

Any kind of vehicle through which commercial communication may be expressed, conveyed or exchanged, or which may enable interaction with the relevant audience.

In 1964, Marshall McLuhan [6] famously stated that 'the medium is the message'. This has been widely misinterpreted by many advertisers as meaning that merely exposing consumers to a message carried by a medium is the primary catalyst for successful advertising. As a consequence of this, much of the focus in media planning over the past few decades has been directed at optimising the volume of communication exposure, rather than maximising the impact of the content and the subsequent return on media investment (ROMI).

McLuhan, however, went on to clarify that 'the content of any medium is always another medium'; in other words, content, context and channel are symbiotically fused elements in any communication outcome. In a world where media and content distribution are ubiquitous, we are increasingly coming to understand that, in practice, the idiom should instead be that the message is the medium, or at least that it is the message that should determine the right medium, or mix of media channels, for inclusion in a campaign.

These principles are clearly articulated in the WFA Media Charter:[7]

Advertisers expect their messages and advertisements be planned and executed in the right media, at the right moment in time and space, to reach the agreed target effectively and efficiently.

There is a growing awareness that it is the context in which consumers are exposed to both channel and content that is most often the catalyst for consumer engagement. In this sense, consumer engagement, rather than nominal exposure, is the true measure of effective communication. It is increasingly being recognised that one of the most critical factors in generating engagement and breaking through the general advertising haze, is relevance.

Quantum leaps in digital technology and predictive algorithms, which process massive amounts of big data at unfathomable speed, now make it possible to deliver unique messages to the consumer's own preferred media device (a practice sometimes known as hyper-personalisation) at the right moment in time and space to maximise the probability of engagement.

Growing concerns about the abuse of personal data and the infringement of consumer rights have led to restrictions being put in place to govern this practice. In South Africa specifically, the purpose of the POPI [8] Act of 2013 (Protection of Personal Information) is, inter alia, to give effect to the constitutional right to privacy by safeguarding personal information and to regulate the manner in which personal information may be processed.

Beyond external legislation, today's media consumer increasingly self-regulates the media platform and content interface and exhibits low tolerance for commercial communication that interrupts or impedes access to any chosen content. This is encapsulated in the advertising adage, don't interrupt the thing I'm interested in, be the thing I'm interested in, and is often manifested in ad-avoidance techniques, also known as ad-blocking, such as fast-forwarding through television advertisements, switching radio stations or subscribing to premium advertisement-free platforms.

In 2015, Microsoft [9] reported that the average human exhibits an attention span of eight seconds. This represents a decline from 12 seconds in 2000. At first glance, this might challenge the viability of advertising as a marketing tool, but the report goes on to clarify that consumers have become far more adept at extracting information and encoding it to memory in shorter bursts of focused attention. In other words, what used to take the consumer 12 seconds to evaluate for relevance and response, now takes eight seconds.

This is particularly evident among digitally connected consumers (digicons) [10] aged 15—24 in South Africa. In this group, total online television and video viewing (81%) exceeds traditional live television viewing (57%) and 89% watch some form of time-shifted television or other user-generated online VOD (video on demand) content or TVOD (television on demand). In this segment, while 58% still claim to watch DSTV, 44% claim to stream an advertising-free platform such as Netflix [11].

This growing focus on media selection is aimed at not only generating the optimal volume of campaign exposure, but also delivering that exposure in the right context. The South African media and marketing landscape is dynamic and constantly evolving. Marketers use technological advancement to drive quantum innovation in consumer interface. Consumer behaviour is also constantly responding to that change. The media planner of the future will not only be required to measure the number of consumers a campaign reaches, but also the number of consumers who are reaching out to that campaign.

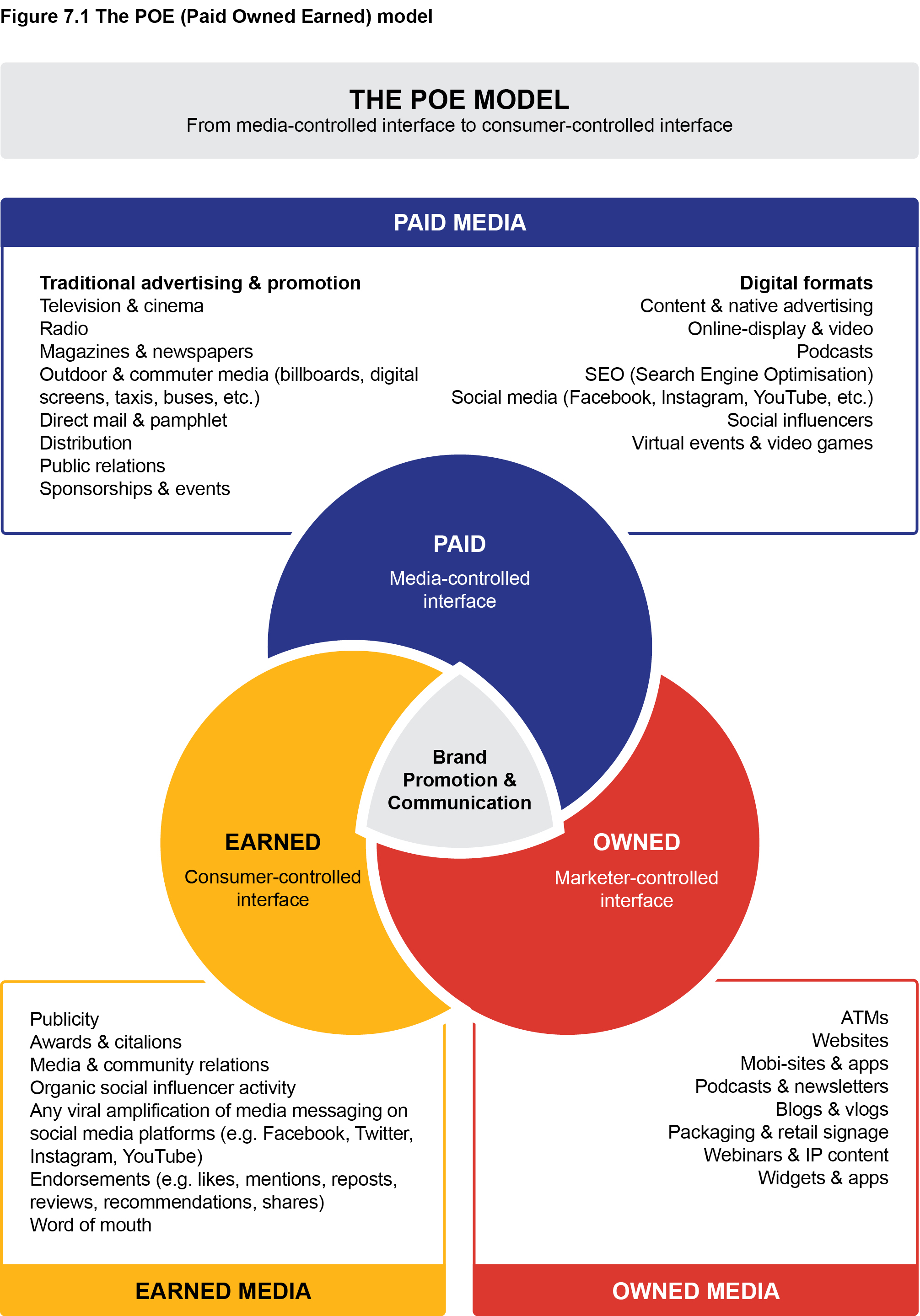

Media channels: The POE model

In the pre-digital era, brand communication and promotional advertising were heavily reliant on what is often referred to these days as 'traditional' or 'mainstream' media. In 1994, when the first cellphone was launched in South Africa, television (39%), radio (13%) and print media (magazines 16% and newspapers 23%) accounted for over 90% of all advertising investment.

Today, 92% of adult South Africans have a cellphone [12], and traditional media now account for only just over half the total communication investment (see Table 7.4). In many instances, advertising has been supplemented, or even replaced, by a range of digital communication platforms and offerings from websites and mobile apps, to social media, such as YouTube, Facebook, Instagram and Twitter.

The POE (Paid Owned Earned) model (Figure 7.1) is widely used to classify and position the various media channels and platforms. The model also reflects the shift from traditional media offering, by which media owners dictate the parameters of the advertising exchange through static advertising units (AU) such as a page in a magazine, or a 30s television or radio commercial.

In this Paid Media scenario, the media planner would determine the viability of the advertising channel by computing the cost of the AU relative to the reach offered by the audience. The relationship between the cost of an advertisement and the size of the audience is referred to as the cost-efficiency of the medium. The cheaper the AU, or the larger the audience, or both, the more cost-efficient the media channel becomes.

Marketers are no longer reliant on only traditional media channels to communicate with consumers or customers. All advertisers have a range of established promotional assets, many of which are powerful communicators. These are collectively referred to as Owned Media. Every time a customer uses an ATM or a banking app, the bank is presented with a unique opportunity to communicate with its customers. Every time someone visits a website or goes into the retail store, the branded marketer has a unique opportunity to reassure an existing customer or persuade a potential customer.

These Owned Media options are significantly more cost-efficient than reaching these same consumers via paid traditional media.

Consumers can search, research and plan their own holiday destination online, and then take a virtual walk through their accommodation before booking directly online on Airbnb. Potential new-car purchasers can take for a virtual test-drive the vehicle they have just seen driving down the road or download an app and opt-in for new product alerts and special offers. In this scenario, marketers control the consumer interface to a far greater degree than was the case with traditional media exposure.

Earlier in this chapter, it was noted that media planning is evolving beyond merely measuring the number of consumers a campaign reaches, towards the measurement of a campaign's in-market stickiness and impact, towards measuring the number of consumers who are reaching out to that campaign.

It is in the Earned Media category that this strategic orientation is manifested. Paid Media are traditionally evaluated in terms of their ability to cost-effectively deliver exposure to audiences. That is, to deliver the proverbial eyes on screen or ears on the radio. Earned Media reflects the degree of momentum, beyond the initial reach, that a campaign is capable of generating without additional cost to the marketer.

Initial infatuation with massive numbers of browsers on the internet, and the high reach implicit in those numbers, was soon replaced with redirected focus evaluating interaction with internet advertising, or the number of clicks that a campaign generates. A campaign with a high click ratio (i.e., the number of people interacting with the advertising as a proportion of the number of browsers incidentally exposed to the advertising) would be deemed successful. A campaign with a high purchase-to-click ratio, even more so. The most successful media campaign will always be the one that produces an in-market response and generates a positive return on media investment (ROMI).

From a campaign audience perspective, the perceived contribution of Earned Media on digital media platforms has moved beyond clicks, and positive contributions are increasingly being measured in terms of other metrics such as the number of likes or shares. Such unsolicited endorsement from a relevant and trusted social influencer, whether it is a positive product review or a simple thumbs-up, builds campaign credibility and overall positive brand attribution.

The more of this positive organic or viral amplification a campaign generates, even from the general public (making the communication go viral), the more effective it is perceived to be. The media landscape never remains static and is rarely, if ever, linear in terms of the way it plays out. Many, if not most, of the established social media platforms, like Facebook, Twitter, Instagram and YouTube, are now trying to monetise their content by offering a range of paid advertising formats. Skippable and now even non-skippable pre-roll videos are ubiquitous on YouTube and most social media platforms. The Carousel ad-format on Facebook lets you show two or more images, videos, headlines and links or calls to action in a single paid ad. Promoted tweets and interactive ad-polls abound on Twitter. Increasingly, social influencers will charge advertisers for endorsements and tweets.

In view of this significant trend, we can now reflect many digital media channels, previously reflected exclusively as Earned Media, as the new form of Digital Paid Media.

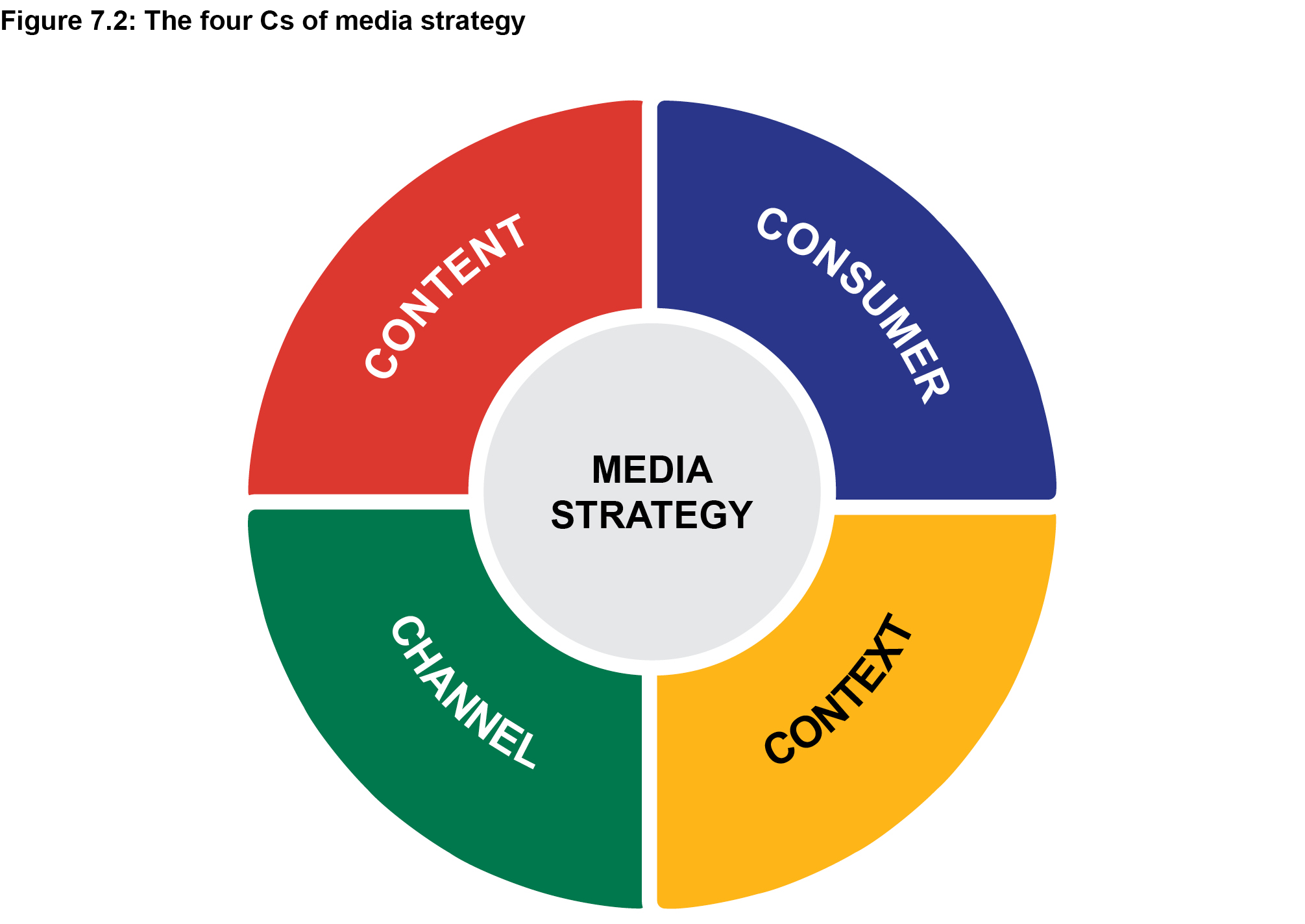

The four Cs of media strategy

Traditionally the focus of media planning has been on measuring the output of the medium in isolation; that is, the size of the audience delivered. This audience currency is often reported as media reach against a specified market segment.

As the divide between digital media and traditional media closes, that narrowing will further dictate that, when planning a media campaign, we need to always apply four simple considerations for ensuring the media mix goes beyond delivering impressive volumes of audience and also enhances and amplifies the creative content.

The four Cs is a framework designed to maximise the effectiveness of any commercial communication by integrating the advertising content (the message), the channel (the medium) and the context through which that content is delivered to consumers, as depicted in Figure 7.2.

Content: Always assess the message that is being communicated and the content space into which the message is being placed. Far too many media plans are being developed without the media strategist even having sight of the creative messaging.

Channel: Develop a media mix that will enhance the impact of the creative content and, where possible, heighten the consumer's sense that the message has been personalised (that is, that the desired response is 'this message is really being directed at me').

Context: Go beyond measuring the number of people who are nominally exposed to a medium and evaluate the context in which the advertising content is being consumed. Consider not only what media is being consumed, but also the when and where of the medium under consideration (the right moment in time and space).

Consumer: Understand the consumer and understand not only what media the consumer utilises, but why it is being consumed. Recognise that consumers are incredibly adept at simultaneously managing channel platforms and content. Cost-efficient delivery is always a desirable procurement consideration, but ultimately the efficacy of a campaign is measured in terms of a positive in-market outcome.

In short, the media strategist is trying to model holistic consumer engagement with hyper- personalised campaign content, which is delivered in the appropriate context, not just quantitatively measuring the volume of audience by any media channel.

It is often said that 'for whales, there is only one ocean'. Equally, it might be said that, for consumers, there is only one campaign.

Media segmentation in South Africa

In order to maximise returns from media expenditure, the consumer landscape is usually segmented into a number of pre-determined groups against which media consumption is measured (See Chapter 11 for more detail on segmentation). Such segmentation can be conducted using any number of criteria considered relevant to the marketer. For instance demographic criteria, such as age, income level or gender.

Geographical distribution is also widely used to create such segmentation. This type of segmentation allows for marketers to decide how much money to spend targeting each form of media (consumed by certain consumers). For example, a local radio station like Alex FM (focused in and around the Alexandra community in north-eastern Johannesburg) has a particular reach (listenership) and marketers wanting to target that community would like to know details about who listens to the station and when.

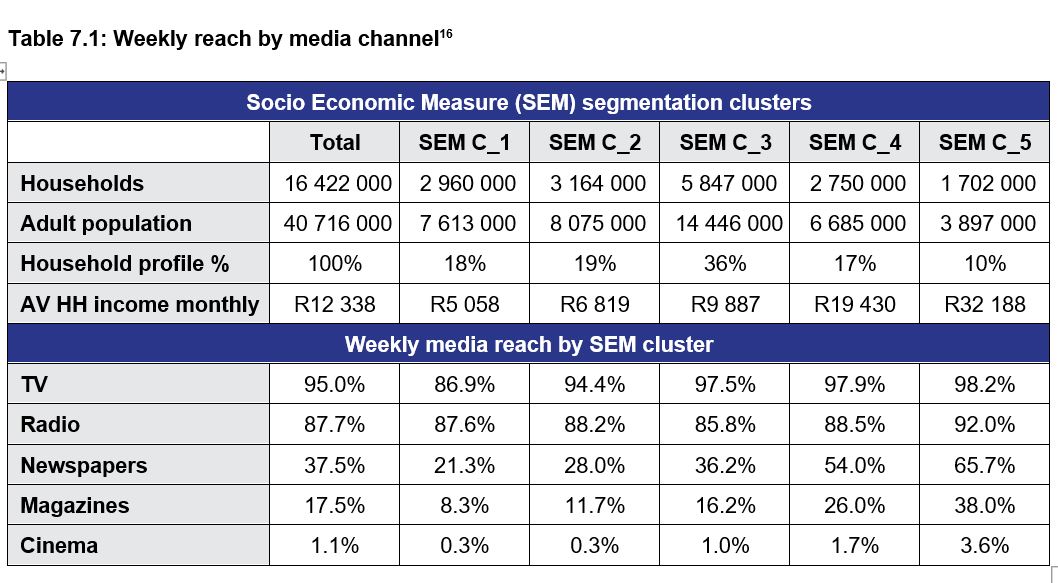

In South Africa, there have been a number of transitions in the way that the media landscape is researched and segmented from a macro socio-economic perspective. Currently, a segmentation tool known as the Socio Economic Measure (SEM) is widely used as a benchmark for broad socio-economic segmentation.

The SEM measure is based on a weighted analysis of 14 key household attributes, ranging from size of house and type of building materials used in construction, to number of appliances in the household and access to amenities such as running water and flushing toilet. Other lifestyle indicators, such as home security systems and ownership of a motor vehicle, are also built into the segmentation model. The SEM model has increasingly displaced the Living Standards Measure (LSM), which has been widely used in South Africa over the past few decades.

At a statistical level these specific SEM household attributes differ from the variables used previously to create the LSM model but, as the South African market evolves and changes in the coming years, these criteria will in turn be adjusted to accommodate the new market realities. At a functional level then, SEM merely represents the most recent iteration of a national socio-economic segmentation model.

Table 7.1 reflects data from the Establishment Survey 2019AB and maps out the SEM model by way of five clusters (broad segments). The top portion of Table 7.1 gives a per-cluster view of the national distribution of households, adult population (15+ years) and average household income. The segments range from the SEM cluster_1 (average household income of R5058) to the top-end SEM cluster_5 (average household income of R32 188).

The lower portion of Table 7.1 reflects weekly reach, per cluster, of a typical set of media channels.

The data in Table 7.1 show that so-called traditional media (magazines, newspapers, radio and television) continue to offer high levels of reach across the full spectrum of the South African market. Reach by radio and television, in particular, remains substantial across the board, while magazines and newspapers still offer viable and focused market penetration from SEM Cluster_3 upwards. Cinema, on the other hand, remains an increasingly niche offering at the Top end of the SEM segmentation scale. In fact, in many respects it is increasingly more useful to think of cinema attendance as an activity rather than a medium in the traditional sense.

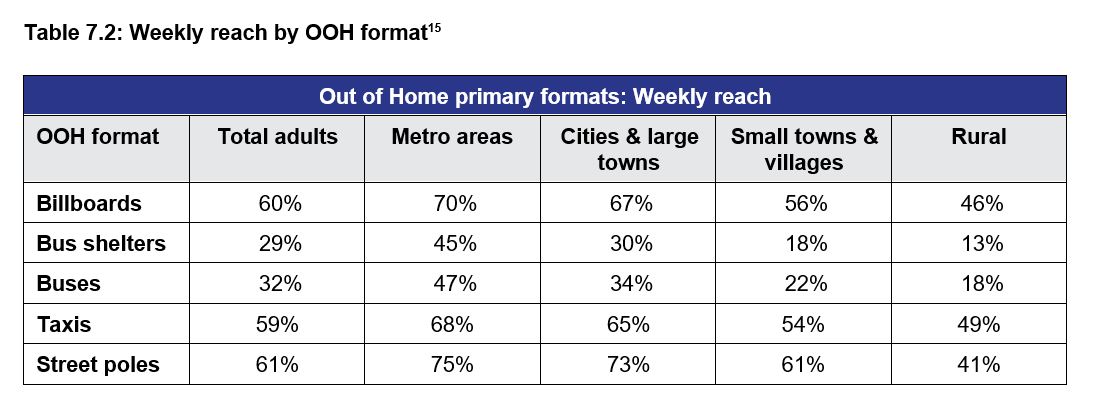

While not represented in Table 7.1 (because the Establishment Survey (ES) does not research this specific advertising format) marketers are also able to measure the reach parameters for out-of-home (OOH) media formats, such as billboards or street poles. AMPS2015 (All Media and Product Survey) demonstrates the OOH medium's ability to reach all sectors of the South African marketplace.

The OOH format reach-distribution represented in Table 7.2 shows that major metropolitan areas are the strongest delivery points for OOH; 70% of consumers in these areas are exposed to billboards and 75% to street-pole advertising, but this reflects the concentration of advertising activity rather than any latent communication deficiency in each platform. There are more OOH sites and opportunities in metropolitan areas than in rural areas, where development may be stifled by a lack of advertising investment.

The diminishing reach offered by transport media from metropolitan to rural areas is a function of the concentration of typical commuter populations in urban areas. In recent years, a growing amount of the advertising placed in these transport media channels has been directed not at external vehicle signage visible to passers-by, but towards passengers, through in-vehicle commuter radio, television and other content initiatives which are increasingly enabled by the rollout of wi-fi infrastructure.

The media mix

Historically, most media research in South Africa has been directed at unpacking the unique contribution of each medium in isolation, so that each media channel could map its own unique audience and maximise the supposed commercial benefit. Until 2017, newspapers and magazines measured readership of printed copies only. Radio stations only measured listenership to broadcasts on a radio set. Television stations measured viewership on a television set.

In practice, this has tended to maintain inflated audience estimates for traditional media channels (or media platforms, as they are increasingly being referred to). These traditional media channels are, however, rarely used in isolation and would typically be combined in varying ratios (known as the media mix) to create a media plan or media schedule. The media mix is the combination of communication channels used in any given advertising or marketing campaign and typically includes a variable selection of television, radio, newspapers and magazines, out-of-home (OOH) media, such as billboards or taxis, as well as websites, email, digital and social media.

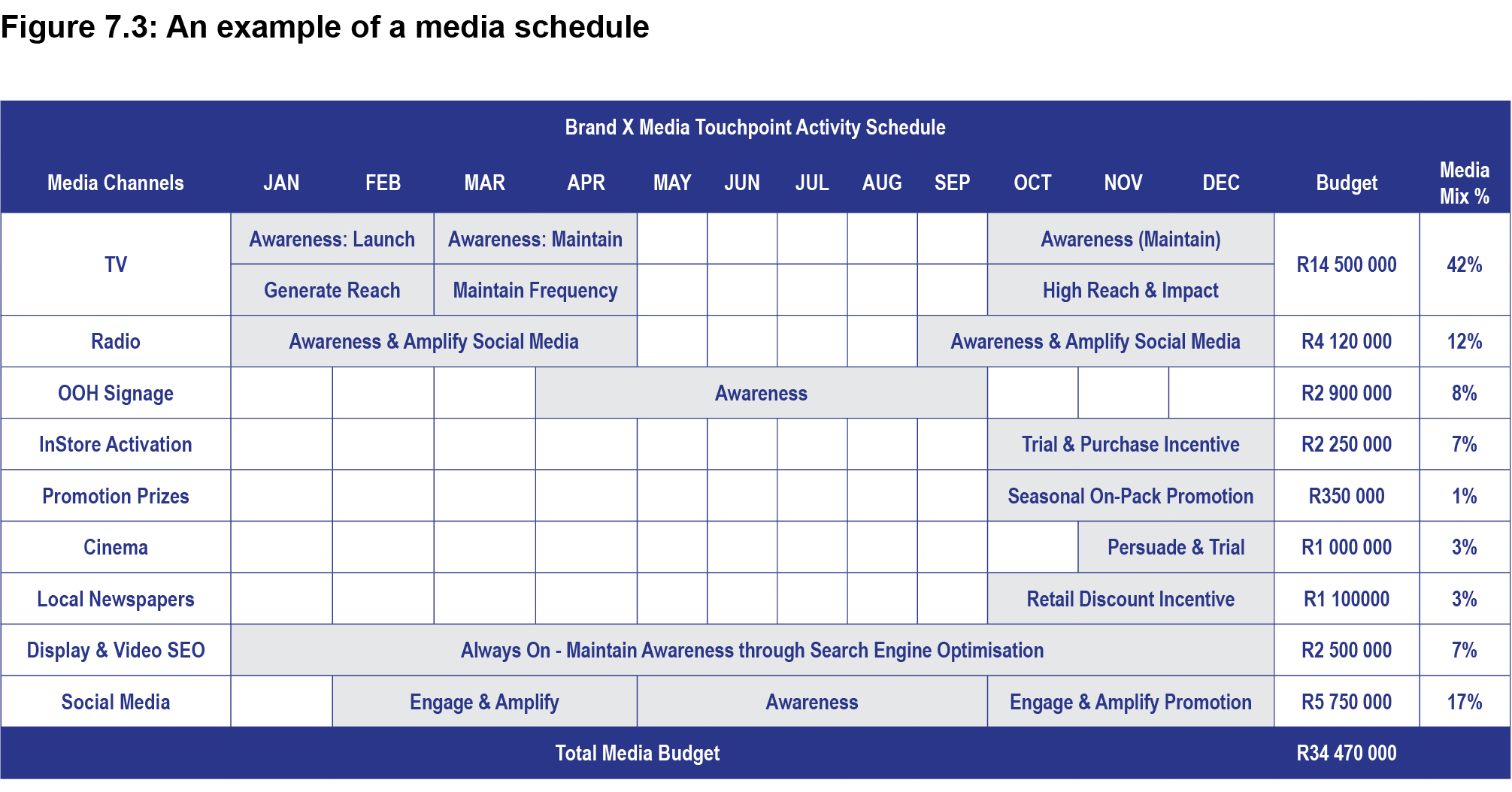

The media schedule is the detailed flow plan of all activities collectively comprising the media plan, and which would typically include the date and cost of planned advertising events as well as the anticipated audience delivery for each element of the campaign (see Figure 7.3 for an example of what a basic media schedule might include).

Each additional medium might be utilised, not only to build additional reach (referred to as cumulative reach) or frequency of exposure against a predetermined market segment, but also to unlock the inherent qualities of the medium in order to amplify the communication content. For instance, cinema might appear to offer little by way of cumulative reach to a television campaign, but when combined with television, it might allow cinemagoers to sample the television-advertised product or even receive geo-located mobile messaging for a future purchase. In this sense, it facilitates personalised engagement.

In an increasingly digital media landscape, however, in which both media channels and content are ubiquitous, we need to shift the emphasis from measuring traditional media outputs in silos to measuring holistic consumer media behaviour. We need to be platform agnostic in understanding how unique media habits shape a consumer's interface with content. It is of no particular significance whether a consumer hears a radio commercial on Metro FM or whether that same audio commercial is flighted on Spotify, Google Play or Soundcloud. The message is the medium and the medium is merely the distribution channel.

Often an analysis of the time spent with each medium can provide significant insights into the consumer's predisposition towards the various media channels. Some consumers tend to read more content; we can refer to them as reading imperatives. Some consumers prefer to listen; they are listening imperatives. Other consumers are relatively heavy watchers of content and are considered to be viewing imperatives.

Some market segments have a higher level of OOH mobility, such as people who have cars or people who are employed and commute to work on a daily basis. These segments have a higher probability of being exposed to OOH. The vast majority of consumers do everything. They read. They watch. They listen. They engage. Moreover, very often they do it all at the same time, or at least with no behavioural consciousness of shifting across channels.

Smartphone penetration and cross-platform media

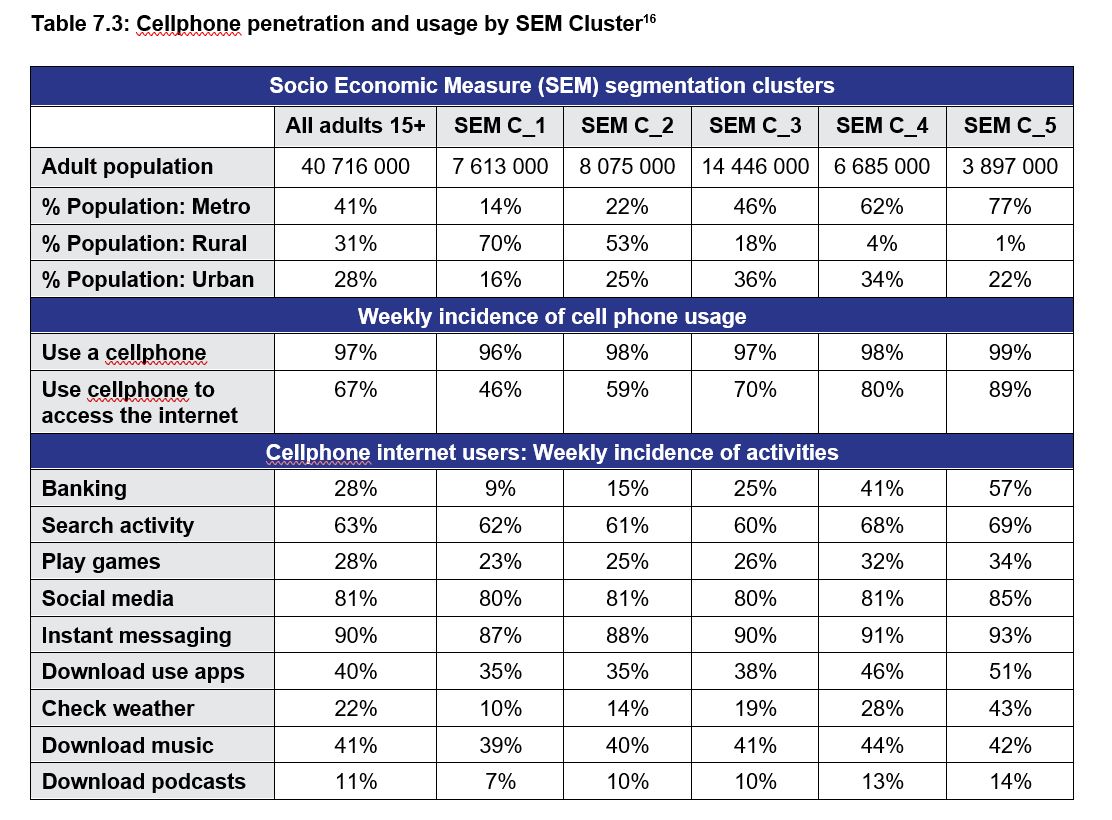

The single biggest contributor to the availability of content across platforms is probably smartphone penetration and access to internet data (see Table 7.3). On average, 97% of adult South Africans make regular use of a cellphone and 67% use that device to access the internet at least on a weekly basis. Even more remarkably, 96% of adults in SEM cluster_1, a market segment which is 70% rural, make use of a cellphone on a weekly basis, while 46% use their cellphones to access the internet weekly.

For those consumers who do use a cellphone to access the internet each week, online activity is not just restricted to search (63%) and encompasses a wide range of other activities, ranging from banking (28%) to gaming (28%) and social media (81%). In total, 41% of digitally connected consumers (digicons) download music each week, with podcasts (11%) becoming an increasingly significant media platform. In South Africa, 90% of all digicons make use of over-the-top (OTT) services, such as WhatsApp. OTT media services are streaming services that offer audio, video, and other media content to viewers, listeners or cellphone users via the internet. OTT bypasses traditional broadcast, satellite or cellular delivery platforms.

Considered collectively, these data highlight the growing importance of media consumption occurring at the time and place, and on the platform, of the consumer's choice. Each one of these consumer activities represents a specific media communication opportunity for the media planner.

Advertising investment telling a story

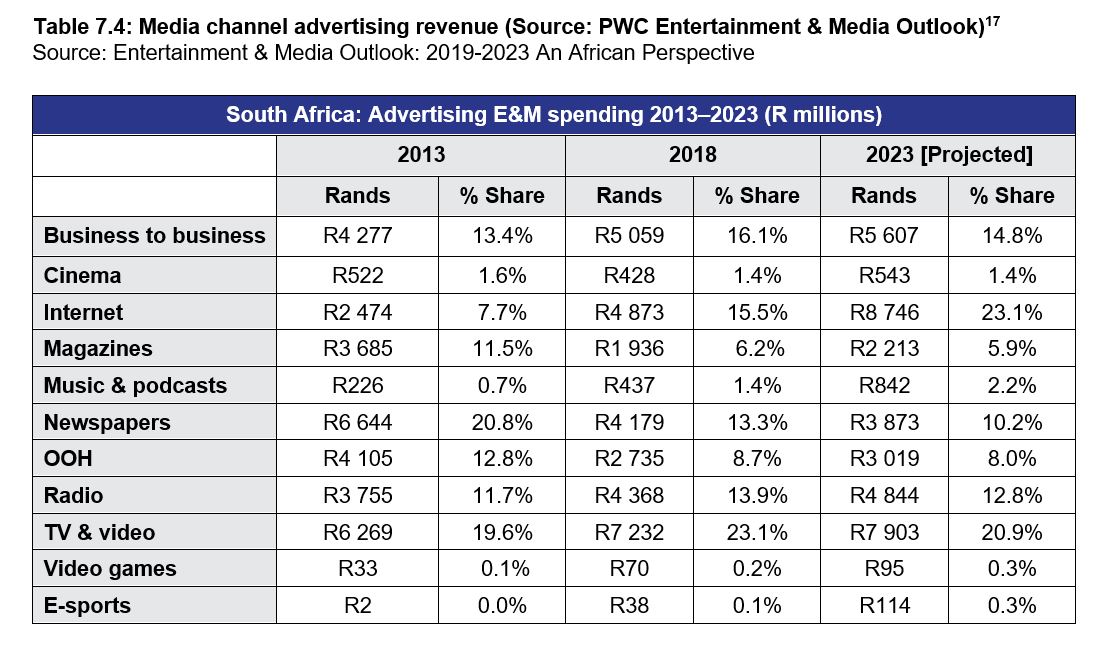

The high incidence and usage of cellphones to access the internet does not mean that the so-called traditional media no longer have a significant contribution to make to media strategy. Most consumers maintain a balance between traditional and digital media formats. Analysis of advertising investment in South Africa highlights the central role of traditional media channels in the media mix (see Table 7.4).

In South Africa, the top 10 advertisers alone invest in excess of R8 billion annually out of a total advertising expenditure of R40 billion in traditional media.[18]

It is worth noting not only the volume of advertising spend, but also the variations in the media investment patterns (the media mix) across a selection of the top 10 advertisers in South Africa. Given that advertising budgets generally remain fixed, they represent a restraint on total media investment and the final media mix always reflects some level of trade-off between media channels competing for that advertising investment.

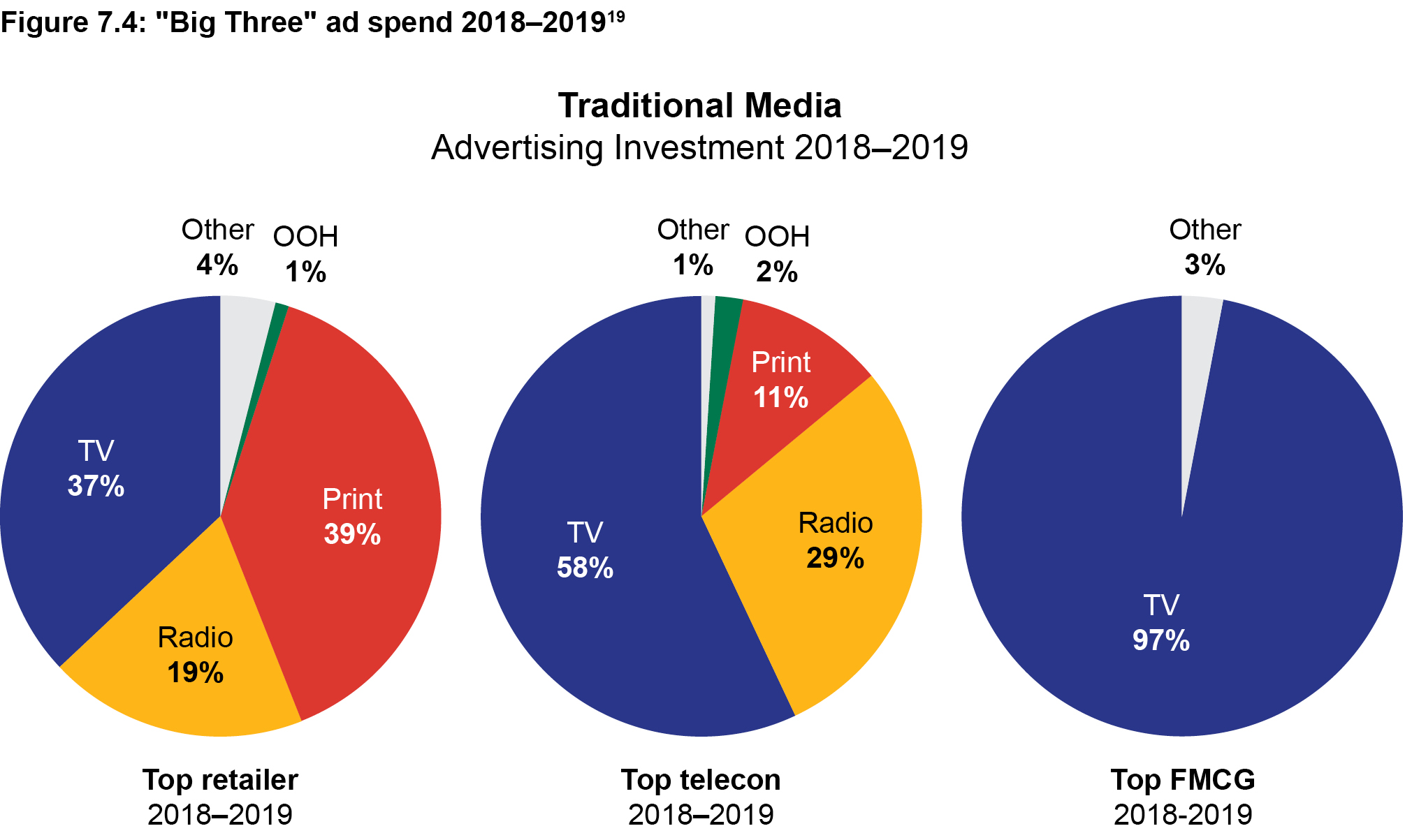

An analysis of ad spend for South Africa's top spenders across three major categories in 2018-2019 (Figure 7.4) reflects the dynamic tension which exists inherently in every media campaign.

The top retail spender shows elevated levels of investment in print relative to the top FMCG (fast moving consumer goods) advertiser. Much of this investment is clearly visible in the form of loose inserts in major and local newspapers at month-end.

The FMCG spender's relatively light investment in other media channels, on the other hand, facilitates an 'always-on' approach to television with 97% of advertising budget invested in that medium. The top telecon advertiser maintains a far more balanced media mix, with a notably higher investment in radio. This is not surprising, when one considers the role of the cellphone in listening behaviour in South Africa.

Each one of these variations in the media mix represents a unique strategic interpretation of the media landscape by advertisers and a unique media response to a set of marketing and communication objectives.

For instance, there is no doubt that the impact of the COVID-19 crisis has shaped the global marketers response to media investment. Many marketers responded to the global pandemic by dramatically reducing or even cutting advertising budgets completely. Others adhered to the traditional view that advertising investment during a downturn is the catalyst for rapid recovery.

Consumers, many of them restricted in their social movements or working from home during lockdown, reflected sharp increases in consumption of digital media, and this may well continue into the future. Warc [20] (World Advertising Research Center) reports that globally the amount of time spent watching online video content quadrupled during the COVID-19 outbreak.

A global average of four hours and three minutes per day was spent watching online videos in April and May 2020 (the peak of COVID-19 for many countries), compared to just 58 minutes in August 2019. What did, however, remain constant throughout this disruptive period was the need for a strategic response to advertising in an ever changing marketplace. The Warc Future of Strategy 2020 report [21] highlighted that 68% of advertisers claim to need strategists more during times of uncertainly. Correspondingly, 94% of strategists claimed that their clients commissioned new strategic work during the COVID-19 crisis: an even higher proportion than those who looked to new creative content as a response to an advertising need.

Even prior to COVID-19, the media landscape had changed inexorably. To talk about the digital landscape to the exclusion of other traditional media platforms is, however, premature and ignores the layered and increasingly holistic reality of the South African consumer's media-consumption habits.

Digital engagement blurring between channels

Digital media do not exist as an alternative to traditional media, but to an increasing degree represent the primary platform for facilitating consumer engagement across all established media channels. As indicated previously, this engagement takes place in the form of simultaneous media channel consumption and, in itself, represents a significant form of embedded ad-avoidance. In total, 92% of all digicons claim to engage in social media activity while watching television and 67% claim to do this on a regular basis (daily or almost every day). South African media research conducted by Nielsen [22] also confirms that the concept of the 'lean-in' viewing experience on television, when every advertisement flighted is an opportunity to see the message, is obsolete.

This growing realisation that media strategies should be developed from a holistic perspective is clearly reflected in significant changes to the parameters of media audience research in primary industry studies, such as ES (Establishment Survey), PAMS [23] (Publisher Audience Measurement Survey) and BRC_RAMS [24] (Radio Audience Measurement Survey).

The revised definitions used by these studies to define reading, viewing and listening audiences reflects an evolution in the way in which the industry views and plans traditional media. For instance, PAMS no longer restricts research to the readership of printed copies of a publication, whether it be a magazine or newspaper, but has widened the scope to include readers who view or otherwise engage with the published content online.

The same applies for listening and watching that is now researched from a behavioural perspective, rather than being restricted to a traditional media platform. Listening audiences include all forms of listening, whether that occurred via a traditional radio broadcast or a streaming digital platform on a cellphone. Viewership is no longer measured in terms of exposure to a television set but includes all digital media platforms capable of delivering video content.

There is a significant growth in ad-avoidance behaviour and time-shifted viewing, often in the form of binge viewing, and this is the new normal. In a digital landscape, viewers can determine for themselves when it is the right moment in time and space to indulge their viewing preferences.

In a media landscape in which a publication and a radio station might both be consumed simultaneously on the same mobile device, or where proximity to a billboard might trigger a hyper-personalised content offering on a linked digital platform such as Facebook or Instagram, the traditional media-silos approach becomes irrelevant. In reporting viewing audience, globally and in South Africa, accepted best practice is now to aggregate audiences for any video content. In other words, not to only report on how many people saw the television commercial on SABC, DSTV or eTV, but also how many people saw the video on Facebook, YouTube, Twitter and Instagram.

Conclusion

In this chapter, we briefly surveyed some core concepts related to the media landscape in South Africa and globally. Consumer marketers and media strategists need to keep tearing down the silos that continue to represent media consumption as a series of disconnected events and recognise the seamless reality of media consumption in a digitally driven landscape. This phenomenon can only accelerate as we increase the bandwidth of the data pipeline into the country and reduce the cost of accessing those data.

Both of these initiatives are very much part of the planned medium-term economic revival of South Africa and these are the infrastructural catalysts which will begin to eradicate the digital divide between all communities in South Africa.

The smart cities of the future, which are already being conceptualised as key drivers in the renewal of the South African economy, will use big-data-derived information and communication technologies to improve service delivery, disseminate information to the public and generally improve the welfare of all its citizens. In the future, unrestricted access to affordable data will have the same status in the South African constitution as every citizen's inalienable right of access to education and water.